To all my readers and followers, although it has been a long time since I have made posts here in the NomadInvestor blog, I have actually been very active in value investing all these while, constantly learning more and doing more of value investing, and it has been an amazing journey.

The reason why I have been silent here is that I have moved on to partnering with a friend and producing content and sharing about investments in another platform — MoneyWiseSmart, where we provide online courses on investing and investment research, with the aim to share what we know about investment and financial education with the other people, and to grow our knowledge and wealth together.

If you are interested in learning more about investments, I strongly encourage and am delighted to invite you to follow us at the following channels. We share a lot of free useful content and also paid courses for those who want more. Cheers all 🙂

Trailer video for our first online course ‘Investing Fundamentals, Financial Statement Analysis and Business Valuation’ launched today (with attractive early-bird price until 9 January 2020): https://www.youtube.com/watch?v=afGiRXSs9Cc

Over the weekend (19-20 January 2019), I attended Value Investing Summit (VIS) in Kuala Lumpur with my investor friends. This is my second time attending VIS (do check out my last year’s post here, if you haven’t), albeit on a sponsored media pass this time and at a place that required much travelling (I am based in Singapore).

This year’s learnings are more about simple time-old wisdom, but these are the ones that are true wisdom that stand the time, and I will be sharing just the key lessons here.

The summary is that:

figure our your investment philosophy and strategy, and have a good process (which I think most should have done so, if you have been investing and learning seriously for a few years); and

more importantly, execute that strategy and process with DISCIPLINE, ROBUSTNESS (don’t slack and ignore things that you know you should be thinking or finding out, but don’t due to indolence), a RATIONAL MIND and PATIENCE, bearing in mind the cognitive biases that human are prone to and always staying HUMBLE and ACT accordingly.

Investing is simple, but not easy. So remember to adopt a simple process and execute it seriously.

Take a simple idea and take it seriously – Charlie Munger

Now, let me turn to some of my learnings in more detail (by speakers), which probably might shed more colour on what I mean.

Vishal Khandelwal (Safal Niveshak)

First, the one year challenge! (I am looking older, but he is the same LOL)

Vishal is a fan of reading and re-reading and re-reading the supertext, instead of reading more and more new things. And hence the lessons that I got reminded from him are those simple time-old wisdoms, which despite simple are very important and impactful.

The points that struck me this year mainly relates to:

the importance of having that margin of safety ALWAYS;

thinking more about and focusing on the risks (that can lead to capital loss) than chasing for upsides (if you take care of your downside SERIOUSLY, the upside will come) – Remember: Getting to the top is optional. Getting down is mandatory;

not taking risks that can wipe you out, like the Russian roulette game;

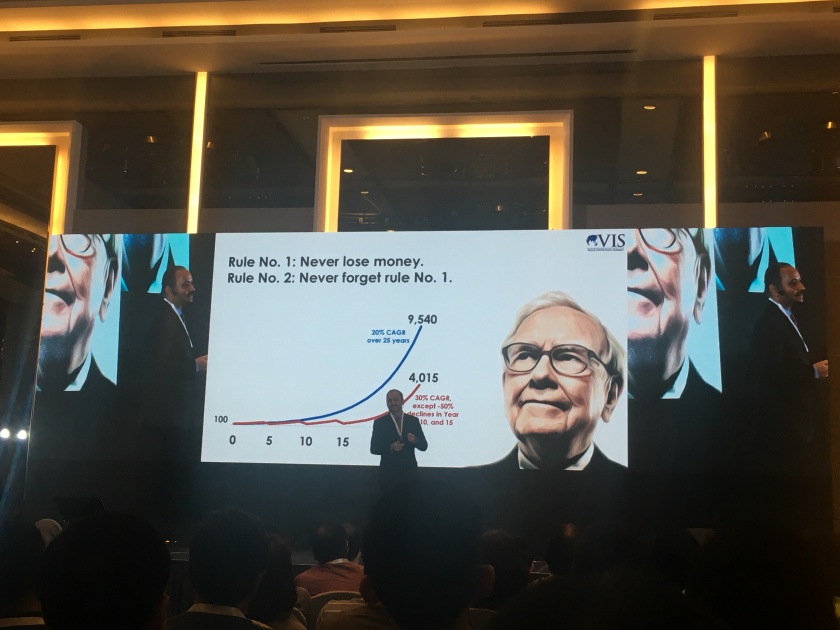

not losing money (the other speaker, which I discuss later, have just 3 down years out of 22 years, which allowed him to keep compounding well); and

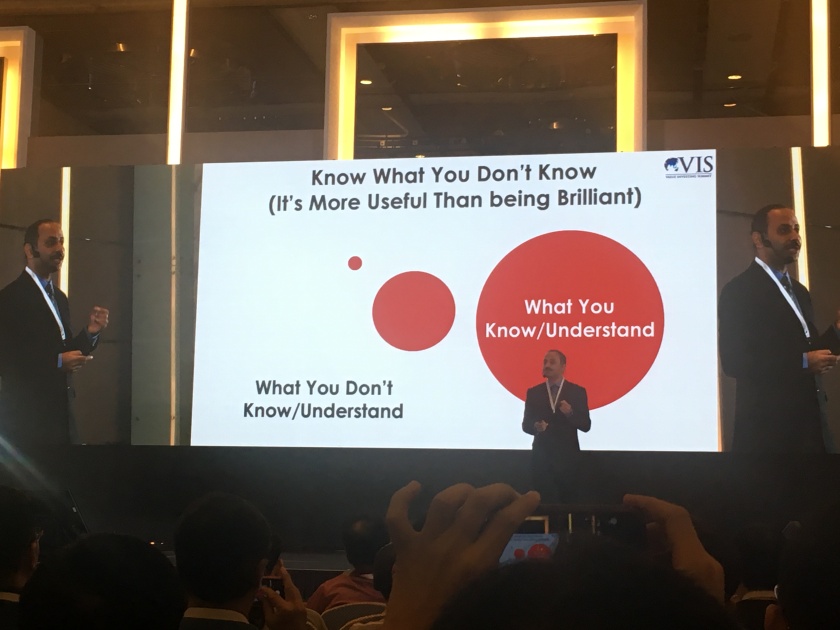

always being conscious and truthful about you own circles of competence and the boundaries of them, and being humble enough to stay within those circles (that’s a higher probability way of having your thesis right, which in turn hopefully leads to higher chances of earning money).

I know we hear this often enough, but there’s a reason why it is constantly repeated by the Oracle of Omaha. So it’s worth reminding ourselves again until we have it fully imprinted like a tattoo for life (just kidding).

Rule #1 – Never lose money. Rule #2 – Never forget rule #1. (And don’t be a swelled head!)

Dr Niwes Hemvachiravarakorn (The Warren Buffett of Thailand)

This is my first time meeting and hearing from Dr Niwes – a very funny and down-to-earth guy indeed, despite having over USD 200 million, after compounding it accidentally from USD 600k for 22 years at a CAGR of 31%. Impressive track records, regardless of whether luck played a role (as he claimed)!

Dr Niwes’ strategy and process are very simple and clear, which I think those who have read intensively in the investing field would have already come across very similar things multiple times.

What makes him successful in my opinion is his ability to execute it well, sticking to the stock selection process with discipline and RIGOUR, and sticking with his SUPERSTOCK companies for long enough with PATIENCE and CALMNESS, which are simple but not easy things to do, requiring a very strong control over temperament and having a rational and dedicated mind.

His strategy and points are very simple, and largely similar to mine.

Investing and getting rich is simple and can be simple;

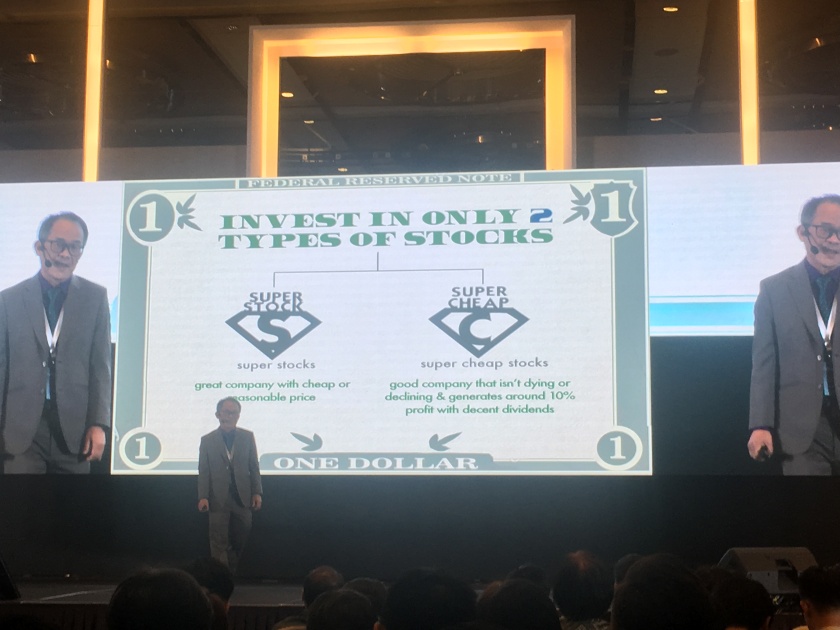

ONLY invest in Super Stocks (hold more than 5 years, aiming for 10 baggers in 10 years), or Super Cheap Stocks (but not in dying industry or with declining profits);

Less than 20%-30% average annual turnover (note: remember punchcard investing, or Mohnish Pabrai’s rule of a strict 3-year lock in upon purchase of a stock);

Look for Mega Trend industry, and the leaders in it, with (i) durable competitive advantages, (ii) virtuous cycles, (iii) good finance, and (iv) good price (P/E less than 30, and low market cap relative to total addressable market (TAM));

And let me repeat, ONLY invest in those, and stick to them strictly and ruthlessly (once you have defined and set up your process and criteria, STICK to them!); and

Just continue living and you will get rich (if you have bought the right companies).

And let me add on – The patience to hold these Super Stock companies through cycles, and give the benefit of doubt to the management (whom you have evaluated to have the ability to know what’s best for the company, in terms of strategy and capital allocation, based on their past track records for decades (and write down these points in black and white, so you know whether the points are really valid or not, and you can’t deceive yourself)) for them to strategise and execute in times of challenges (else you would miss out recoveries and continuous compounding of those companies).

So, please go into buying a company with the expectations that you are not aiming to sell it at the peak before its fundamentals deteriorate for long, but with the expectations of being able to sell it at maybe 70% of its top performance after allowing the company and the management some time to execute to navigate and emerge from the tough times (as no business would have smooth sailings all the time). In other words, before you sell, remember to give the management whom you have identified as excellent executives and capital allocators, and whom you trusted upon your purchase of their companies, some time to correct and execute in overcoming those tough times and crisis, just like what they have done successfully in the past (for multiple times).

Super Stocks! Super Cheap Stocks! Well said!

Overall, Dr Niwes’ presentation makes me believe, and remember, that a good simple strategy and process, when well executed by a dedicated value investor with discipline, can produce tremendous results and wealth over time!

So let us be those dedicated value investors. And do the hard work of executing with discipline and rigour! (Focus on the process, and the outcome will come)

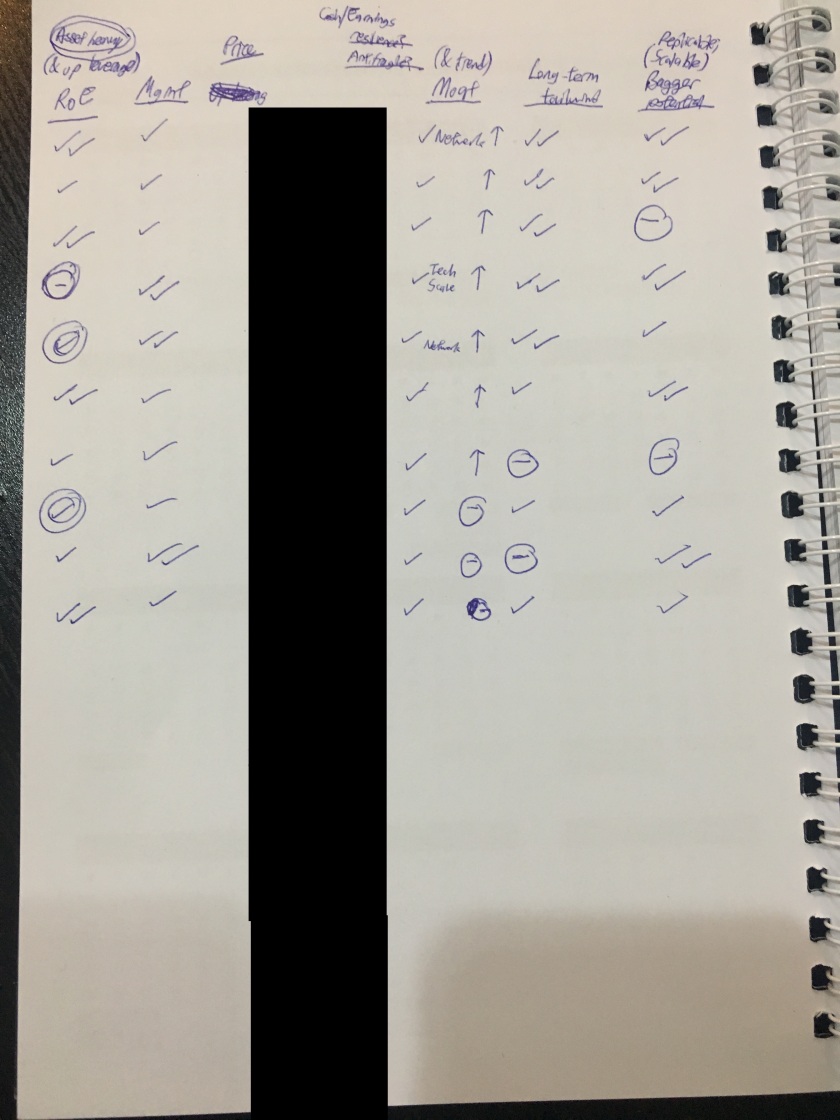

These thoughts of mine that occurred to me then made me think hard about the quality of the companies that I own, on whether they are Super Companies (I would prefer to call them so, then Super Stocks which probably are more catchy) and whether they have the top of the cream qualities on all aspects. So that I don’t sacrifice quality and the opportunities to hold only the real good companies on almost all aspects – if they don’t make the top tier, cut them, and keep turning the stones until you find the top.

Reflecting on the companies I own, on their quality, on whether they are indeed Super Companies… I have found 10, or so I think at least, and I am looking for 10 more so that there are higher chances for a few of them being undervalued at various points of time~ (Please let me know if you have ideas :P)

I managed to catch Dr Niwes for a question that I had before he left, where I asked him, what are the challenges he faced throughout his journey of applying such a strategy. His answer was, not much (he had only 3 down years out of his 22 years journey – impressive! which I believe is achievable if you focus on and remember margin of safety, eyeing on the risks (not the upside), circle of competence and good balance sheets and business models), but probably the challenges were like what he had said, selling too early. And hence his advice, “Keep Calm!”

Me: Challenges? Dr Niwes: Nope. Keep Calm! (And live longer LOL) (Golden advice indeed)

(For record and reference only) Examples of Dr Niwes’ (past) Super Stocks:

CP All – He held since 2009 and would sell when it becomes the largest company in that industry

HM Pro – Sold few years ago, as he saw competition

BH – Best private hospital, with medical/ageing tailwind

BDMS – Same as BH

AOT (Airports of Thailand) – Sold

CPN – Biggest shopping mall

MINT – Hotel group

Other learnings

Charlie Tien, the founder of Guru Focus, read and re-read Buffett’s letters from 1950s to now for multiple times, which changed his life. He also made reference to Wilshire 5000 Total Market Index, to GDP ratio, as an indicator to look out for market cycles. Some of his ideas/companies include Church & Dwight (dealing with household products in the US) (note: seem to be a compounder and have reduced share count over the last few years), and Kweichow Moutai (bought first in 2014 at 8x P/E, when Xi Jinping became the leader and started on anti-corruption campaign).

Joshua Zhang, investment manager at HCF, on spotting (and avoiding) fraudulent and fishy companies, especially Chinese ones, which I think are very important in avoiding losses, so it’s an interesting and useful topic for me (e.g. on different ways to tunnel money out). And invert thinking can come in handy here.Sarah Fu 傅喻, the only Asian reporter to interview Warren for eight consecutive years and founder of 喻见 Media. Again, same resounding principle. Master one basic principle and follow it strictly!Jack Kouzi (or Jacuzzi) from Australia – Director of Strategy at VFS Group. Interesting top-down macro selection strategy, and views on Alibaba (including on its India expansion)China – The growing massive economyPanel Q&A. Question: Rebalance after a company becomes multi-bagger and big portion of portfolio? Vishal: Yes. I would keep all companies at <15% of portfolio by market value (he suffered major losses from his over-concentration of 80% in a stock that didn’t do well before). Charlie: Not really. I wouldn’t, but depends on company. (Nomad Investor: I am more, or totally, aligned with Vishal – no right or wrong, just personal preference)Joshua Zhang, investment manager at HCF, on spotting (and avoiding) fraudulent and fishy companies, especially Chinese ones, which I think are very important in avoiding losses, so it’s an interesting and useful topic for me (e.g. on different ways to tunnel money out). And invert thinking can come in handy here.

Some interesting case studies are:

HIK Vision – it has been in my list of companies to study for quite some time, and at this point I am still conscious of its overseas growth (due to sensitivity of security products) and wouldn’t include much of it in performing a valuation of the company for margin of safety.

Fast Retailing – Story sounds good, growth in international markets could be there, with moat (on use and advancement of technology and intangible assets), but ROE is not showing up as well.

Yihai – Interesting to learn about 张勇. Might have issues with payables and receivables.

So that sums up my key learnings for this year’s VIS~ Hope you have enjoyed the event and this post. And thank you to the organisers for extending the media pass to me!

Next year’s VIS would be in Kuala Lumpur again on 11-12 January 2020, so do check it out if you are interested~

P.S. And do feel free to discuss with me (by sending a message to Nomad Investor, or at my email at thenomadinvestor@gmail.com) if you have any ideas to go into my Super Companies list 🙂

P.S. And do check out another great article on VIS 2019 from MoneyWiseSmart here if you haven’t.

Finally got to see Mount Fuji when I was leaving the area on the last day~

Recently I went to Japan for a week for travel, in particular to Tokyo and the Mount Fuji area (Hakone – Gora and Fuji-kawaguchiko).

The first thing that stood out to me when I touched down on Tokyo Narita airport was that I saw Fanuc advertisements everywhere on the trolleys at the airport. Lol. Fanuc is a great company which I have analysed two months ago in August 2018, after a friend of mine brought my attention to it.

And the interesting thing that happened was that when I was in Japan, due to probably escalated concerns over US-China trade war and rate hikes, Fanuc’s share price came down even more, despite already crashing ~30% from the peak this year, which got me more interested.

So, here’s a brief write-up on Fanuc. And do visit my friend’s post on Fanuc too if you are interested.

Fanuc is the world leader in CNC (computer numerical control, i.e. the brains to control machines) and industrial robots. A Japanese company established in 1972 as a spin-off from Fujitsu, it is currently run by the son of the founder. It has commanded more than 50% (up to around 60%) global market share in CNC for decades and around 25% of global market share in industrial robot arms.

Let’s start with two videos that give an overview of Fanuc and its products/services, first one in 2016 and second one in 2018.

Fanuc is one of the Big 4 of industrial robots (together with Switzerland-based ABB, Japan-based Yaskawa, and German-based Kuka). It’s prowess and leadership in industrial robots are both shown in the demand side (largest in CNC, largest in terms of number of robots installed, top 3 in various segments of robots, good branding and reception by customers due to good quality, reliability and service (it stocks much more inventory than the competitors, and it replaces a faulty part in the customer’s factory instead of repairing there, to reduce down time); and the supply side (it’s fabulous production model of producing standardized parts (including rejecting customers’ highly customized orders), building on proven past technology (instead of drastically new ones), to leverage on existing knowledge curve and reduce the number of parts involved, issues with reliability and changes to production lines.

These are shown in its operating margins north of 30%-40% (comparable or even higher than Apple even though it is asset heavy!), significantly higher than the other Big 3 that has between 4%-12% operating margins. What’s more is that Fanuc achieved this on slightly lower selling price of its products than its competitors. So Fanuc’s products, although not using the most innovative technology, are cheaper, proven, reliable, and come with good service (lifetime management and at least 25 years of spare parts available, even for parts for machines no longer produced). And reliability and good and fast services are very important in production plants, where downtimes can cost a bomb (can be tens of thousands of dollars per minute for some customers).

Fanuc has achieved what GM and GE set up to achieve many years ago, to automate the factories worldwide, but failed terribly (after spending lots of money and high-performance management resources), and are now partnering with and helping Fanuc to sell its products (and using them too). Fanuc’s production plants are mainly in Japan (mainly around Mount Fuji – where Fuji eruption is quite a significant risk that can wipe out its factories) and some of them are lights-out factory, i.e. no lights and air-con are turned on because there is no one inside the factories (it’s just lots of robots producing lots of robots, to the extent that the mother robot has to be tied with clear markers so people know which robot is producing which, given the fast speed of movement of robots).

Industrial robots market is picking up now, projected to grow at ~15% for the next few years (so there is sufficient tailwind for the leaders, with increased pie shared by them), given improvements in technology and increase in labour costs in leading manufacturing countries (especially in China, where robot density per production worker is still extremely low). And deep learning, AI and IoT are picking up, and Fanuc has a head start in 2016 (with Cisco, Rockwell Automation, etc), in terms of linking all the robots and machines in its customers’ factories to collect and process all the data (to predict when a robot is going to go down, and thus scheduling maintenance promptly, reducing downtime), and improving the yield of the robots (by using AI to make the robots learn how to do things better and coordinate with other robots).It’s FIELD system is an open platform, akin to the App Store on your smartphone, where developers can develop app for different use of the robots or machines linked. And its ZDT (Zero Down Time) application has already been adopted by its customers and saved them millions of dollars of cost savings.

Albeit having a ROIC of 25%-40% (excluding its massive cash of ~JPY 800b (no debt), which is more than half of book value equity), and having just spent massive amounts of capex for factory and production lines expansion in the past 3 years (of ~JPY 100b per year, dwarfing the ~JPY 30b of capex per year in the previous 7 years), in view of the strong current backlogs of orders and future orders, the market has priced Fanuc lower, sending its price down >40% from the peak early this year, and back to 2015 level, due to concerns of slowing down of smartphone sales (of which the robots that help to make smartphone components, including Apple’s metal casings, are about 1/3 of Fanuc’s total revenues) (and probably due to concerns over US-China trade war). This part of Fanuc’s business is tied to the cyclical smartphone cycles, but its order books for other products are still going strong, and in the long term the cycle would go up and down regardless, with an overall structural uptrend.

I see Fanuc still growing (and leading together with the other 3 of Big 4) in the next 5-10 years, riding on this structural uptrend in industrial robots and automation happening around the world (even SE Asia countries, with relatively lower labour costs) are also adopting them now).

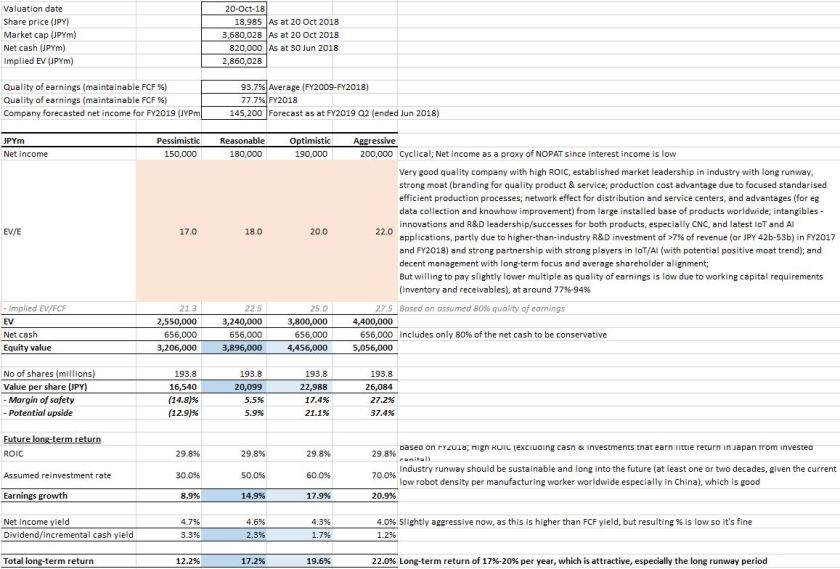

At the current market cap of ~JPY 3.7 trillion, this implies an EV of ~JPY 2.9 trillion, so a EV/NOPAT of about 14x FY2015 (ended Mar) NOPAT (its good year), 23x FY2017, 16x FY2018, or 20x FY2019 (management forecast as at Jun 2018, which is lower than previous years due to slowdown in IT-related industry this year. However, its forecasts tend to be conservative, with it outperforming in the end).

Which can be attractive, from a long-term investor’s perspective, for a high ROIC market leader (3x-10x greater operating margins than largest leading peers based on their firm-wide overall margins (instead of specifically on comparable business segments) with sufficient runway in a market with strong tailwind run by a focused founder-family-management with more than five decades of experience (during the financial crisis in 2009, it shut down its communications with investors, because it wanted to focus on the operations of the business, which some might deem not good).

I personally think Fanuc could reasonably be worth around JPY 3.9-4.5 trillion, or JPY 20-23k per share, and could compound its value at 17-20% a year for the next 5-10 years, based on the reasonable and optimistic scenarios in my valuation below.

My valuation of Fanuc (as at October 2018)

Another interesting development is the acquisition of German-based Kuka by Chinese Midea Group in 2016/2017, after Midea failed to get its hands on Japan-based Yaskawa. After that event, the German auto manufacturers have been gradually switching out Kuka’s robots which are dominant in the German market, to other players including Fanuc, due to concerns of the Chinese obtaining all the data and know-how of German auto production processes (the robots and machines are now collecting almost all info, so if one gets its hand on the robots, it has a lot of data). So even though Fanuc might face tougher competition from Kuka in the Chinese market (which is growly rapidly and has more than enough pie for everyone I believe), it actually benefited a lot from the German market (and it is expanding its European operations there now aggressively), a market with the 2nd or 3rd highest robot density per manufacturing worker in the world (after Korea).

Admiring Mount Fuji, and contemplating the future of Fanuc~ (Mount Fuji please don’t erupt lol)

Hope you have enjoyed the post and Mount Fuji. Do let me know if you have any comments or insights on Fanuc or this industry 🙂

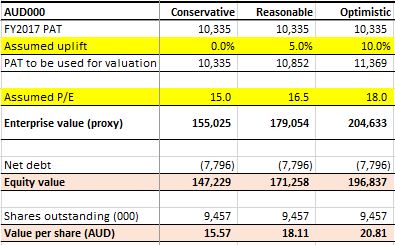

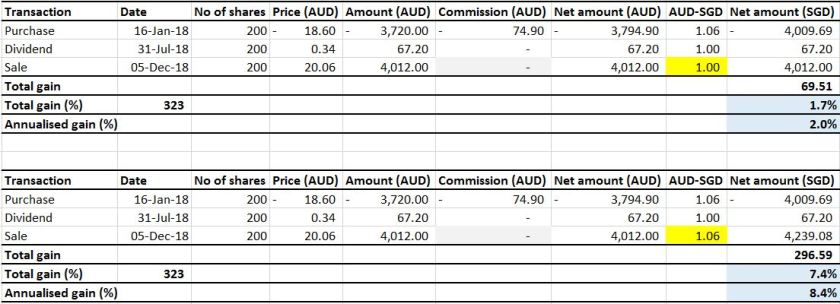

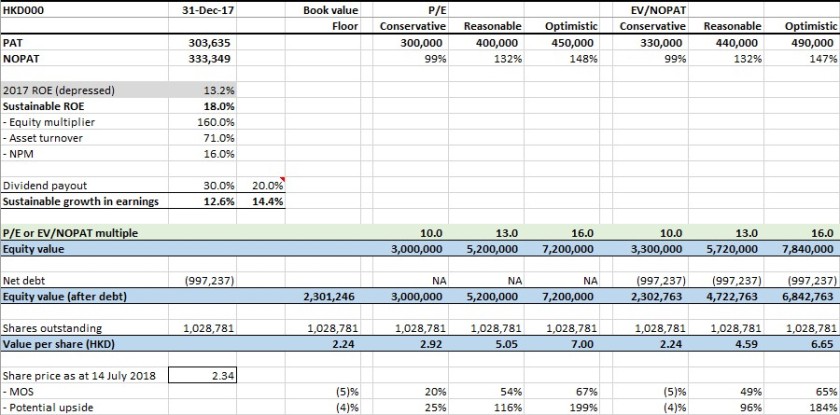

Capilano Honey, a company which I partially owned since January this year, received a take-private offerearly this week. This becomes the second take-private offer I received in my investment journey, after GLP in 2017.

The price? Cash offer of AUD 20.06 per share , translating to equity value of around AUD 190m, with the option to receive scrip shares in the new entity. This offer price represents a 28% premium over the last close price (AUD 15.65) and implies a FY18 P/E of 19.3x (on earnings which I consider to be still depressed) and FY18 EV/EBITDA of 12.5x.

The buyer? A private equity group (Wattle Hill), co-founded by Albert Tse (the husband of Jessica Rudd, daughter of former Australian prime minister Kevin Rudd… LOL), specialising in China-focused agricultural exports.

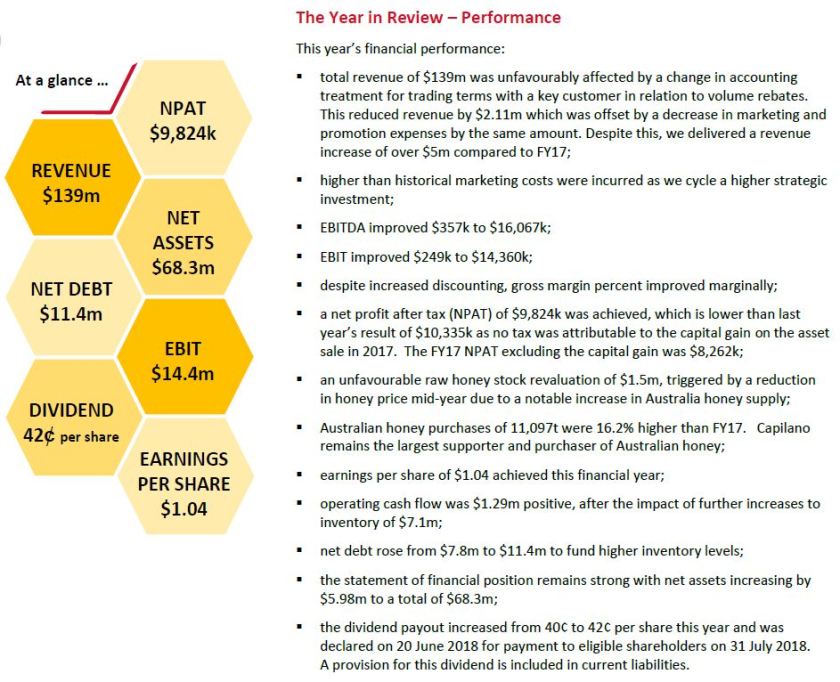

At the same time, Capilano also released its FY2018 results, which were quite good in my opinion.

Revenue increased by 4% to AUD 139m;

Operating profit increased by 19.6% to AUD 14.0m (disregarding the one-off non-operating capital gain of AUD 2.1m last year); and

Honey stock further improving to 6,746 tonnes from 5,953 tonnes last year with better season (although Eastern Australia started seeing increasingly apparent dry conditions in recent months).

Kerry Stokes, who has 21% voting power via Wroxby Pty Ltd, has already indicated to vote for scrip consideration and the deal is likely to go through.

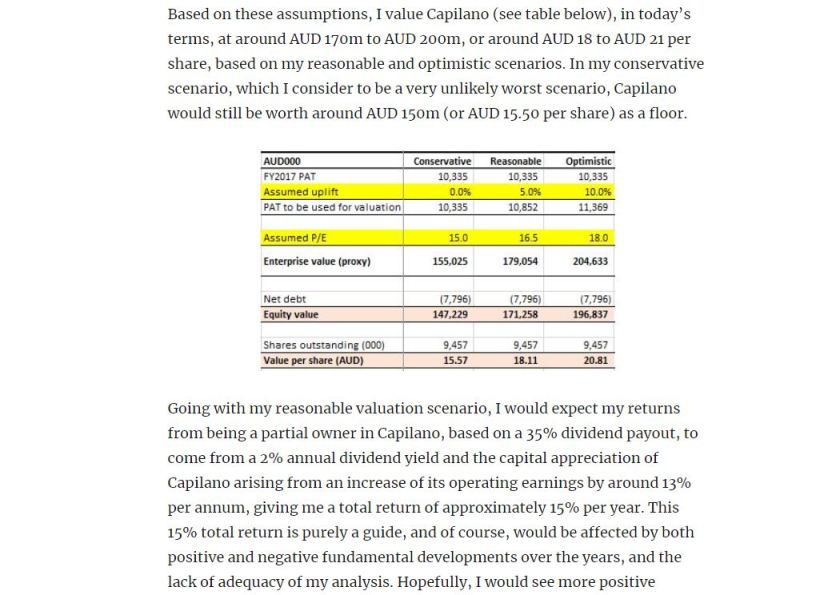

The offer valuation of AUD 190m lies towards the upper range of my valuation of AUD 170m to AUD 200m made in January 2018. And I feel that the offer price could have been a bit higher, at around AUD 200m or even slightly more (given the benefits that the buyer would accrue, from recovery in earnings and likely expansion into China utilisting their expertise and networks).

I purchased it at AUD 18.60 per share, or AUD 176m for the whole equity. And I received a dividend of AUD 0.34 per share in July, so this should imply a return of approximately 10% [= (AUD 20.06 + AUD 0.34) / AUD 18.60 – 1].

But my returns? It depends largely on how AUD performs against SGD in the coming months.

For now, assuming I hold it till take-private happening in 5 December this year and AUD-SGD remains at the current rate of 1.0x till then, my returns would be a mere 1.7% (after taking into transaction fee, of a whopping AUD 75 (or 2% of my purchase cost) from OCBC Securities, which I discovered it to be this high only after I received the transaction statement – I thought it would like in the range of AUD 25 similar to other markets, but lesson learned).

If lady luck is with me, and AUD appreciates back to 1.06 SGD (the rate I purchased in January) by December, then my return would improve to 7.4% (for 10 months), or annualised rate of 8.4%, which is sub-par and below my expectations. Nevertheless, still a good and interesting ride and a first attempt in buying an Australian company.

Given that I am based in a foreign country outside of Australia, with my shares purchased through custodian by my brokerage firm, opting for scrip in the new entity would be risky and unwise for me in my opinion.

So for now, all I have to do is wait for the privatisation to happen end of this year and hope for an appreciation in AUD (I’m unlikely to sell before that, to avoid incurring the whopping high transaction fee charged by OCBC Securities again) (or hope for someone else to come in with a higher bid, which would be a blue moon LOL).

To end my journey with Capilano (I have been following Capilano hashtag on Instagram, joining Australian beekeepers forum on Facebook, checking out Capilano’s products whenever I am in a supermarket, etc), let’s hear back and enjoy this catchy Capilano song! (scroll to 14:53)

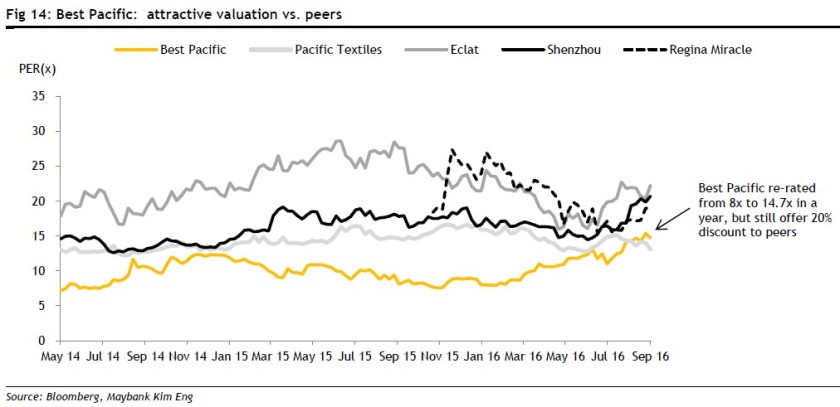

Company name: Best Pacific International Holdings Ltd (“Best Pacific”)

Stock code: HKG: 2111

Market cap (as at 14 July 2018): HKD 2.4 billion

Average daily traded value: HKD 0.9 million

1. Executive summary

Best Pacific is a China-based textile manufacturer of high-performance lingerie and sportswear materials, with a focus on elastic fabric, elastic webbings and lace. It is the world largest lingerie materials manufacturer, supplying to renowned lingerie brands (e.g. Victoria’s Secret, Triumph, Wacoal, Maniform, Aimer, and Spanx) since 2003, and is increasingly expanding its sales to global sportswear brands (e.g. Under Armour, Lululemon, Adidas, Puma, 2XU and Sweaty Betty) since 2013.

Best Pacific fits my investment criteria – a good company with strong lasting moat (Criteria 1), high returns on capital (Criteria 2) and sufficient reinvestment opportunities (or growth runway) (Criteria 3); run by decent/good management (Criteria 4); and available at reasonable/attractive prices (Criteria 5) – and therefore constitutes one of my key holdings which I intend to hold for long (five years or more, as long as the fundamentals and my thesis remain intact).

The following sections set out:

an introduction of the company;

details and my views of the company, in terms of:

its moat (criteria 1);

its return on capital (criteria 2);

its reinvestment opportunities (criteria 3);

its management (criteria 4);

the risks associated; and

its valuation (criteria 5);

some concluding thoughts.

2. Introduction

Overview

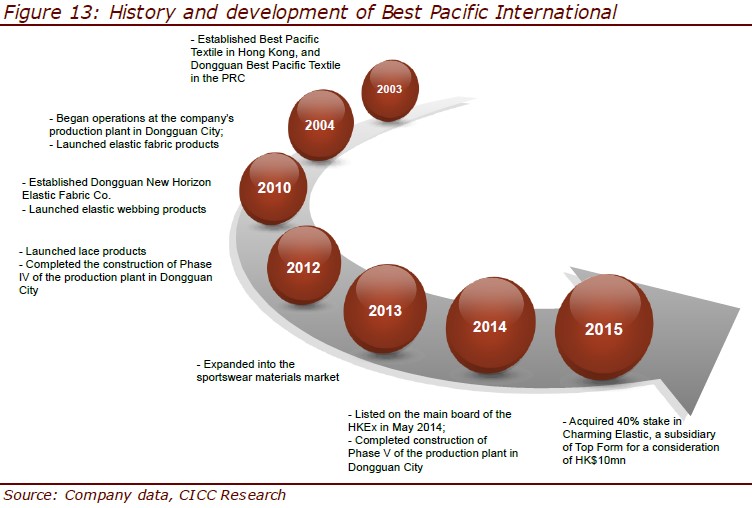

Best Pacific was founded in 2003 by two textile veteran, Mr Lu Yuguang 盧煜光 (current executive chairman) and Mr Kane Zhang Haitao 張海濤 (current CEO), and was listed on HKSE on 23 May 2014, raising around HKD 530m.

In 2004, it began its operations in Dongguan, China, manufacturing and selling elastic fabric products to lingerie players. Subsequently, it progressively expanded its operations, and six years later it started launching more product categories – elastic webbing products (2010) and lace products (2012), becoming a one-stop supplier of the major material components of a typical bra.

In 2013, leveraging on its expertise and knowledge in elastic materials (elastic fabric and webbing), it expanded into a new high-growth market – the sportswear materials market, and the management intends to grow this business segment to a size larger than that of lingerie.

History and development of Best Pacific

Source: CICC 2016 report.

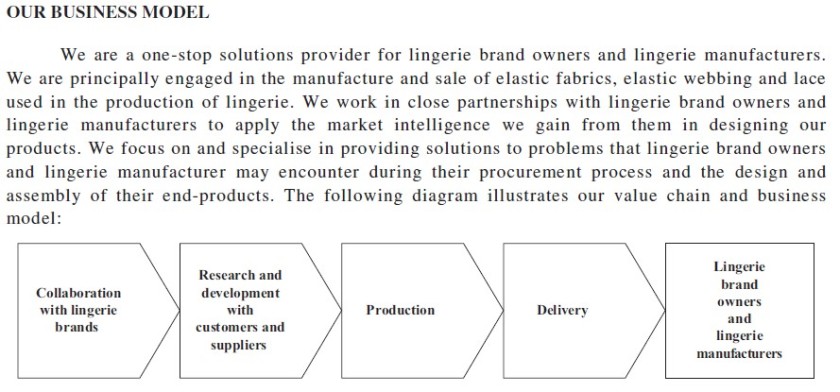

Business model

Best Pacific mainly engages in the manufacture and sales of elastic fabrics, elastic webbing and laces.

Unlike an ordinary OEM (original equipment manufacturer), it works in close partnerships with (i) the lingerie/ sportswear brand owners, (ii) the mid‑/ down-stream garment manufacturers and (iii) the raw material (fibre/ yarn) manufacturers, to apply the market intelligence it gains from them and its own R&D activities in designing its products. This R&D activity, innovation capability and close partnership with other stakeholders in the value chain differentiates Best Pacific from a normal OEM/ ODM (original design manufacturer).

Best Pacific’s value chain and business model

Source: IPO prospectus.

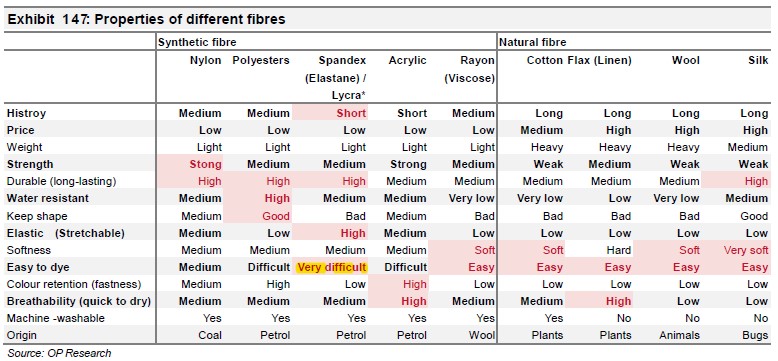

In addition, Best Pacific specialises in producing fabrics using synthetic fibres, in its case nylon and spandex (or also known as elastane globally outside of the U.S., or associated with Lycra which is a common type of spandex invented by DuPont), instead of natural fibres (e.g. cotton and wool). Synthetic fibres have certain advantages over natural fibres, for e.g. cheaper, lighter, more durable, have more strength, and offer more colours, textures and other properties (water resistant, quick to dry, super elastic, anti-bacteria, etc), and there has been increasing use of synthetic fibres (which have a shorter history) in the market. However, compared to natural fibres, they are much more difficult to dye, which is a key process in the production, and therefore requires a certain level of know-how and skills. Thus, contrary to the general impression of commodity-like textile manufacturers, Best Pacific competes not just on price, but also on technology, know-how, innovation and quality in the synthetic materials field.

Properties of different fibres

Source: Oriental Patron 2015 report.

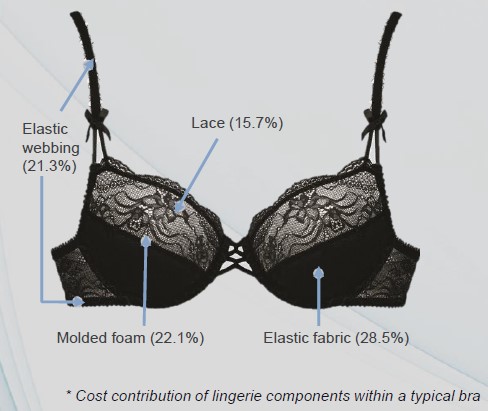

On the lingerie segment, a unique point about Best Pacific is that it is not only the largest lingerie materials provider in the world (more on market and competitors later), but also one of the few players that provide one‑stop solution for the three (of four) major components of a typical bra, in terms of cost – elastic fabric (29%), elastic webbing (21%) and lace (16%). It does not deal with molded foam (22%), but there has been increasing popularity of bralettes which do without molded cups, so for those products Best Pacific is able to supply almost all the components required.

Components of a typical bra

In terms of pricing, Best Pacific generally adopts a cost plus pricing model, which according to the company has enabled it to maintain a relatively stable gross profit margin.

So, in short, Best Pacific’s business model (which allows it to extract economic rents) is that:

it procures textile raw materials and converts them into fabrics which it sells to garment manufacturers or brands, pricing them on a cost-plus basis (where possible) and therefore isolating itself from any changes in raw material costs;

it adds value in the process of converting the materials into fabrics, where it utilises and leverages on its PPE base, know-how/skills/technology to understand the market requirements/trends and produce good quality fabrics and innovations (in terms of raw material innovation and end product innovation) that it has developed over years of R&D, market research and close partnership/relationship with its customers and suppliers. It also adds value on the lingerie segment in terms of being a one-stop supplier of the major components of materials, allowing for easier procurement, quality control and consistency and shorter lead time. These are the main value-adding aspects of Best Pacific, which allow it to earn decent/superior gross profits (ressulting in economic rents); and

it imposes (financial and operational) discipline on itself to control/ minimise the operating costs of the business, for e.g. by controlling labour costs, adopting automation both in terms of production and warehousing inventory control, strategically locating its production facilities close to customers to reduce logistics cost and lead time, etc. In my view, this is a hygiene factor that Best Pacific has to achieve, which does not allow it to extract additional economic rent (since peers would do the same, and in fact can probably do better due to their larger sizes and greater customer concentration (resulting in less distribution costs) and earn above-average return on capital.

Operations

Best Pacific has the following visions and missions (based on its 2017 annual report):

Vision: “Build on innovation and technology” has always been the Group’s vision in developing new products to meet the market demand. Through its dedication in research and development, the Group has developed a diversified portfolio of high-performance lingerie, sportswear and apparel materials, which are blended with quality, comfort and functionalities.

Mission: While Best Pacific is expanding and diversifying the customer portfolio with its innovative products across the sectors, we also focus on delivering our social responsibilities and the Group has always aimed at creating a green, healthy and safe working environment, while at the same time educating and equipping our staff with the relevant skills and knowledge to manufacture safe and quality products. Best Pacific not only sees the mission as part of our high corporate governance and social responsibilities, but also considers it a crucial element for the long term sustainable development of the Group.

In terms of operations, Best Pacific has been based in Dongguan, China all the time, until it expanded into Vietnam (2016) and Sri Lanka (May 2018). As at the end of 2017, it has 6,409 full time employees – 91% (5,859) in China and 9% (550) mainly in Vietnam.

In terms of products, Best Pacific produces three product categories – elastic fabric, elastic webbing and lace.

Best Pacific’s products

Source: Company website.

Source: Company website.

Customers

Since its operations in 2004, Best Pacific has gradually secured several global renowned lingerie and sportswear brands and developed close relationships with them (which in my view goes to showing its quality products and strong capabilities).

Some examples of customer sign-ups include Triumph (2004), Marks & Spencer (2005), Victoria’s Secret (2007), Wacoal (2008), Under Armour (2012), LuluLemon (2013), Adidas (2013), 2XU (2016), Sweaty Betty (2016) and Uniqlo (2018 – tentative, as I have not been able to confirm this yet).

Currently, it has a broad customer base of over 300 customers (according to a 2017 report by Huatai Financial).

Best Pacific’s customers

Source: AlphaLab by Fifth Person.

Source: AlphaLab by Fifth Person.

Source: Maybank 2017 report.

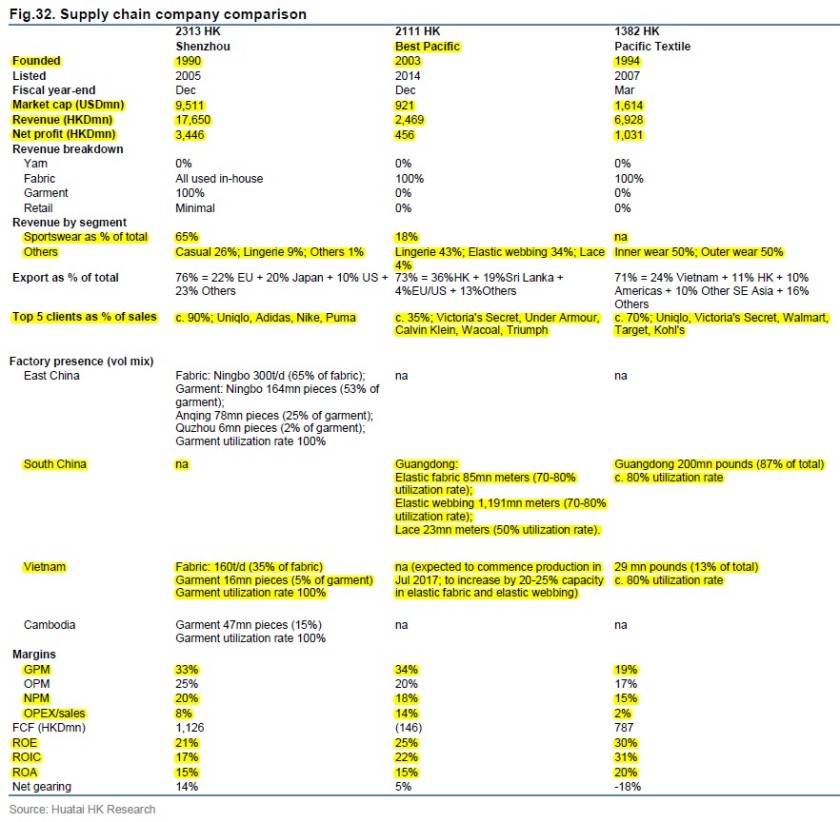

However, Best Pacific has a few key customers that constituted a major portion of its sales, in particular Victoria’s Secret (around 25% for both lingerie (12%) and sportswear (12%)), Under Armour (4%), Calvin Klein, Marks & Spencers, Wacoal and Triumph; and is therefore exposed to the sales performance of those customers. This level of customer concentration, however, is low relative to a few of the other strong competitors/peers (e.g. Shenzhou International and Pacific Textile – more on competitors later) which can have ~70%-80% of sales concentrated in top 5 customers.

Details of Best Pacific’s customers

Source: CICC 2016 report.

Source: Maybank 2017 report.

The images below provide a better idea of the type of end products sold by Best Pacific’s customers.

Products sold by Best Pacific’s customers

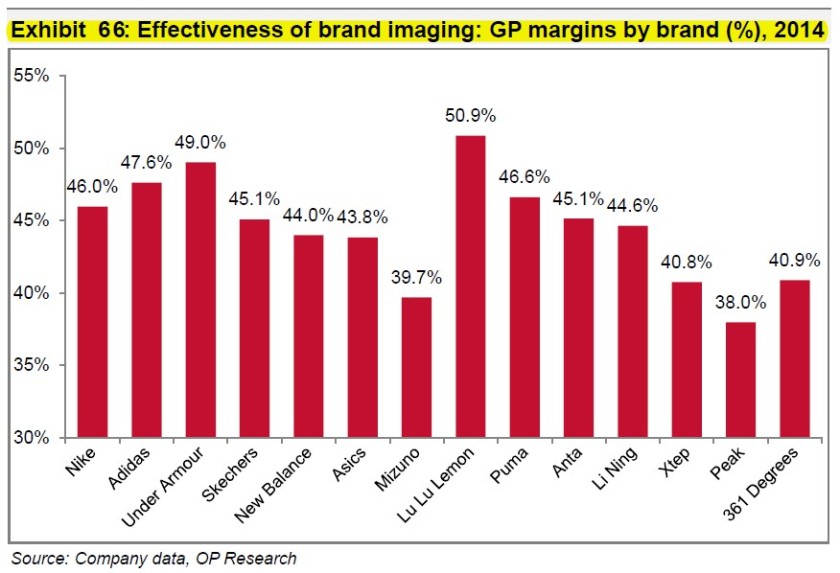

As seen in the figure below (based on 2014 financials), the sportswear brands that Best Pacific works with has relatively high gross profit margins (>45%), which are potential indicators of powerful brands with a certain level of pricing power.

GPM of sportswear brands (2014)

Source: Oriental Patron 2015 report.

Assets & production

As at end 2017, Best Pacific had total assets of HKD 4,215 million (based on book value), with the majority being:

PPE – HKD 2,277m (54%);

Inventories – HKD 694m (16%);

Receivables – HKD 648m (15%); and

Cash and bank deposits – HKD 243m (6%).

The majority of its PPE (HKD 2,277m) was:

machinery (HKD 1,309m or 58%);

buildings (HKD 551m or 24%); and

construction in progress (HKD 357m or 16%).

As seen in its asset base, Best Pacific is operating in a capital intensive environment, with more than half of its assets in PPE, of which around 60% of it is machinery. According to a Daiwa 2014 report, “Since the majority of the machines used by Best Pacific are state-of-the-art ones and are imported from Europe (Karl Mayer machines for elastic fabric and lace, Miller machines for lace), we expect machinery purchases to continue to take up the bulk of the Best Pacific’s capex budget.” The costs of these textile-producing machineries are not cheap (especially for lace). Based on data in the 2014 IPO prospectus, the (approximate) cost of one machine for:

elastic fabric was HKD 0.39m;

elastic webbing was HKD 0.23m; and

lace was HKD 5.32m.

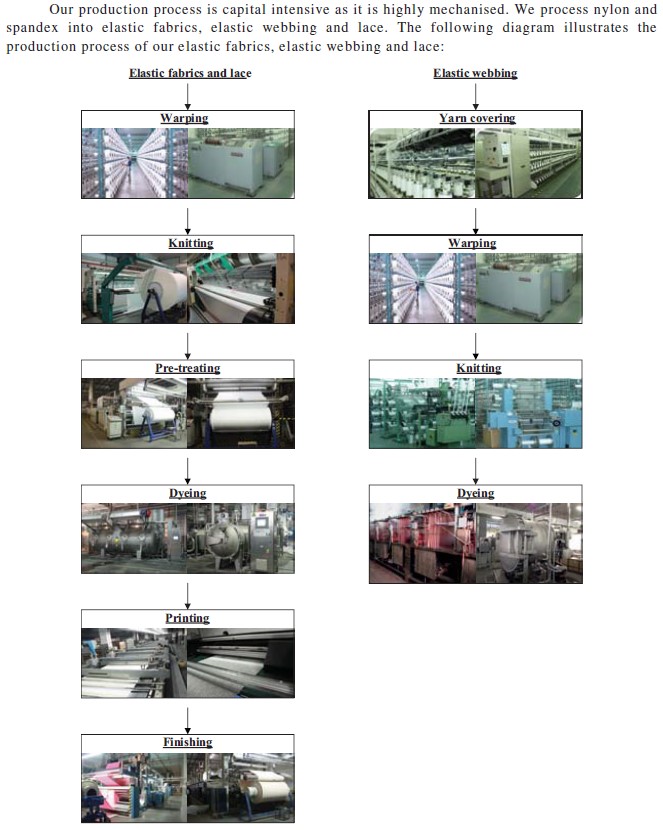

In terms of production, the production process is capital intensive as it is highly mechanised, where the company processes nylon and spande into elastic fabrics, elastic webbing and lace (as shown in the diagram below). The production time from raw material to finished elastic fabrics and lace is ~2-3 weeks and ~1 week for elastic webbing, while raw materials are generally prepared three months ahead.

Production process

Source: 2014 IPO prospectus.

In terms of production facilities, the company has been increasing its capacity for all three product categories greatly over the last few years, more than doubling the capacity from 2013 to 2017 (i.e. a CAGR of 18% or more), partly due to increased capital from its IPO in 2014.

Best Pacific’s production capacity

Source: Annual reports.

Source: Huatai 2017 report.

International production footprint of Best Pacific

Source: Company 2017 results presentation dated 21 Mar 2018.

The diagram above depicts Best Pacific’s international production layout. Up until 2016, all of its production facilities were located in Donguan city in Guangdong province (and Jiangxi province) in China. On the Dongguan plant, China Securities International indicates in its January 2017 report that [emphasis mine]:

“Dongguan plant is running at 24 hours a day, with high labour retention rate. There are a total of 3,000 workers in the Dongguan plant, with production running 24 hours a day on 3 shifts of around 8 hours each. The average monthly wage rate is c. RMB 4,000, which is higher than the industry average. Also, a dormitory is provided in Dongguan’s city centre. As such, the worker’s retention rate after the previous Chinese New Year holidays was over 90%”;

“We are impressed by its high automation production process, making it nimble on capacity adjustment and least vulnerable to wage hike in China, which we believe will be one of its major competitive edges over a shortening order cycle”; and

“At present, its warehouse is operated manually. BP is planning to upgrade it to full automation in 2017. This is expected to enhance its production efficiency and the estimated cost is RMB 100mn.”

In 2016/2017, the company started constructing its first plant in Vietnam, in the VSIP (Vietnam Singapore Industrial Park) in Hai Duong, with a total investment of around HKD 600m, increasing the production capacity for elastic fabric and webbing by ~25%-30% (compared to end 2015). The plant was completed in mid 2017, with the trial production started in July 2017 and the first batch of production conducted in 2017Q3. As at March 2018, there was over 500 staff (~9% of total workforce) employed in Vietnam and the company expected to hire up to 1,200 local workforce in the near future.

According to the company, the reasons for the expansion of production in Vietnam include to leverage on the beneficial tax incentives and the cost savings from lower labour costs and logistic costs, and to be located nearer to its customers (e.g. Regina Miracle (IDM for Victoria’s Secret) and many other brands/garment manufacturers which have been moving their production from China to other countries like Vietnam since early 2010s (mainly in the wake of relatively higher labour costs in China).

Details of Best Pacific’s Vietnam plant

Source: Company 2017 results presentation dated 21 March 2018.

Source: Company 2017 results presentation dated 21 March 2018.

Source: Company 2017 results presentation dated 21 March 2018.

Source: Company 2017 results presentation dated 21 March 2018.

According to a CSI 2017 report, “BP is expected to derive cost savings from logistics (it no longer needs to ship its products to its customers in Vietnam), and lower labour and operating costs (which is 40% lower than PRC).”

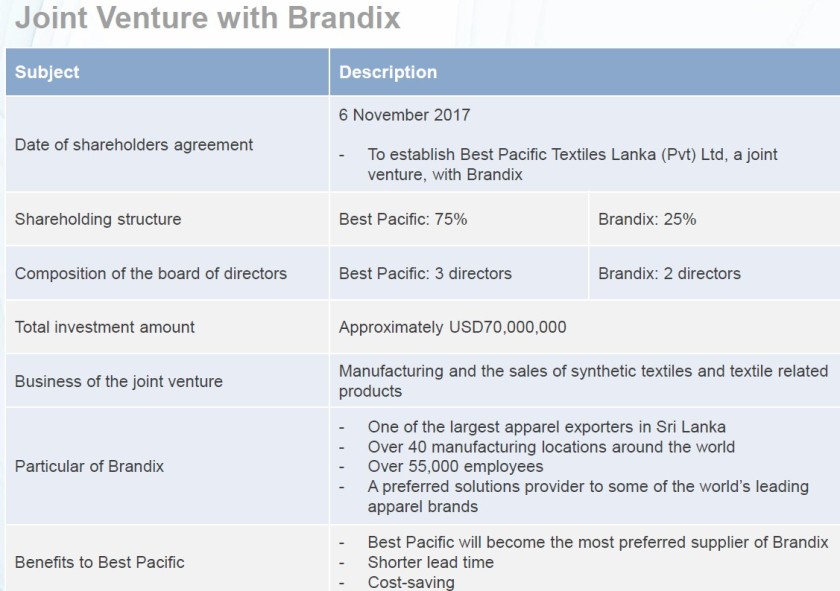

Recently, in May 2018, Best Pacific also started a joint venture with Brandix (Sri Lanka’s largest end-to-end apparel solutions provider (with 55k employees vs Shenzhou’s 75k) and an existing long-term major customer of Best Pacific (with overlapping customer base, e.g. Victoria’s Secret and M&S, and other customers like GAP and A&F)) in Sri Lanka, Best Pacific Textiles Lanka (“BPTL”), to manufacture and sell synthetic textiles and textile related products.

The total capital contribution into BPTL would be USD 70m (or, less likely, USD 50m, based on a different source) from Best Pacific (75%) and Brandix (25%), with some in-kind asset contribution (including main factory building structure and store building structure) of USD 1.5m from Brandix. The JV will be managed primarily by Best Pacific and will produce fabrics (with a specific focus on warp knit synthetic fabric) and supply to Brandix, and Best Pacific would become the most preferred supplier.

According to a DBS June 2018 report, the joint venture would require a new plant and construction should finish by the end of FY18F, which would form a substantial part of Best Pacific’s capex for the year.

Details on Best Pacific’s joint venture with Brandix

Source: Company 2017 results presentation dated 21 March 2018.

A bit more about Brandix – It also has partnership with Pacific Textile (Best Pacific’s competitor) for a very long time since 2004, through a joint venture called Teejay Lankan Plc, which was listed in 2011 on the Colombo Stock Exchange and focuses on knitted fabrics for the intimate apparel and sportswear industries, with its largest clients being Victoria’s Secret, Marks & Spencer and Intimissimi. This joint venture was more of a cotton fabric producer, instead of synthetic, but has entered into the synthetic fiber segment (due to good growth and demand, and to be a comprehensive one-stop supplier) in 2017 (with acquisitions of companies with such manufacturing facility). However, the focus of the synthetic category is polyamite, different from Best Pacific’s nylon and spandex, so I see it as a different and indirect competition. In my opinion, it might be that Brandix does not have the experience/ capability to manufacture the right type of synthetic fiber, including in this JV with Pacific Textile (allthough I am not entirely sure now). Thus, it had to, or it chose to, partner with Best Pacific recently to go into the synthetic nylon and spandex categories. The fact that it chose Best Pacific, and not Pacific Textile or others, was a positive point to me.

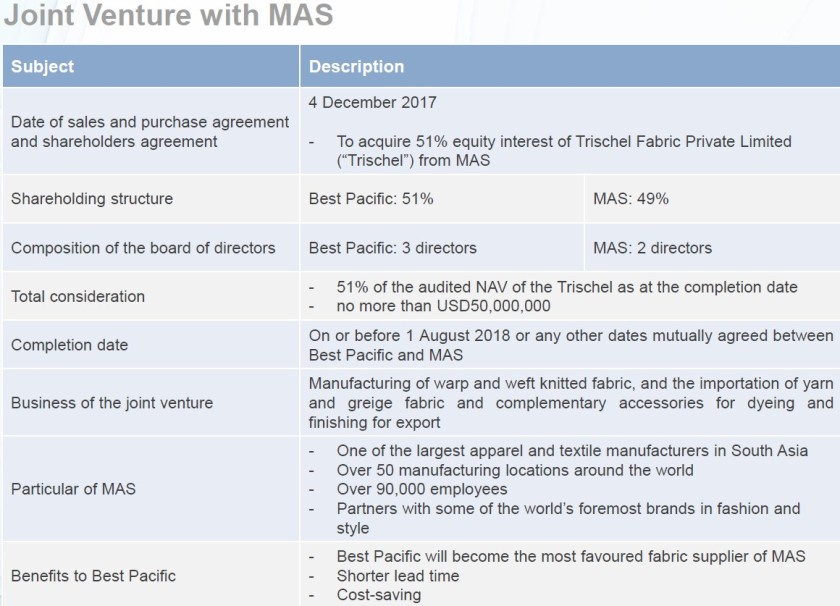

In addition, on 4 December 2017, Best Pacific also entered into a joint venture agreement with MAS Capital (a direct wholly-owned subsidiary of MAS, which is a current major customer of Best Pacific with long-term business relationships, and a reputable leader in the industry of apparel and textile manufacturing with mature international operation systems) in relation to the acquisition of 51% of the total issued share capital of Trischel Fabric (Private) Limited from MAS Capital.

According to the 2017 annual report, “Pursuant to the MAS JV Agreement, the consideration for the acquisition shall equal to 51% of the net asset value of Trischel as at the completion date and, in any event, shall be no more than US$50,000,000. Pursuant to the MAS JV Agreement, the completion of the acquisition shall take place on or before 1 August 2018 or any other date as BPSL (Thulhiriya) and MAS Capital may agree in writing. After completion, Trischel will continue its existing businesses including, among others, the manufacture of warp and weft knitted fabric, and the importation of yarn and greige fabric and complementary accessories for dyeing and finishing for export. Up to the date of this annual report [around 20 March 2018], completion has not yet taken place and Trischel is still owned as to 100% by MAS Capital.”

Details on Best Pacific’s joint venture with MAS

Source: Company 2017 results presentation dated 21 March 2018.

According to a DBS June 2018 report, “BP should takeover the MAS JV in 2H17, which is an existing operating plant. BP has already deployed staff for this operation and minor profit contribution is likely within FY18F. The Brandix JV requires a new plant and construction should finish by the end of FY18F. The majority of BP’s capital expenditure in FY18F would be associated with this expansion.”

A bit more about MAS – It also owns (unclear ownership %) Stretchline Holdings, the largest lingerie elastic webbing maker (5.1% market share in global elastic webbing in 2012, versus Best Pacific’s 3.9%) based on a Frost & Sullivan research. Based on Stretchline’s website, it is the world largest and only branded narrow fabric manufacturer, with many (patented) innovations (LockSafe, Fit-J, BondeLast, Stay4Sure and Fortitube technologies, which are lock-knit, narrow fabric, silicone coating, or puncture resistant fabric wirecasing technologies).

Materials & suppliers

The primary raw materials that Best Pacific uses in its production are nylon and spandex (around 70% of all raw materials based on a Daiwa 2014 report). The company also sources dyes from the suppliers. The cost of raw materials form a large part of the company’s cost of sales, at around 50%-60% in the past five years (2013-2017). It purchases these raw materials mainly from suppliers in China, Taiwan, Hong Kong and other overseas countries, which are manufacturers and sourcing agents of nylon and spandex.

Based on the 2014 IPO prospectus, the company has had business relationships with its five largest suppliers (which constituted around half of its total purchases, which has seen come down to 36% in 2017) for long periods, ranging from four to 10 years. Based on a Daiwa 2014 report, the company’s main suppliers include:

Korea-based Hyosung (004800 KS) – Best Pacific partnered with Hyosung to launch a new range of fabrics with MIPAN Aqua X and creora Fresh (with moisture management, UV protection, comfort, fit and freshness from odour neutralising technologies) at ISPO Munich in February 2017;

Japan-based Asahi Kasei (3407 JP); and

Japan-based Toray Industries (3402 JP) – which has become a substantial shareholder of Pacific Textile in early 2018, the closest competitor of Best Pacific.

Based on my own research, I have also identified working relationships between Best Pacific and other suppliers, i.e.:

US-based Eastman Chemical Company (NYSE: EMN) – Best Pacific produces Naia-based fabrics which are hypoallergenic, breathable, have a silky luxurious drape and hand-feel, and have good printing properties; and

US-based Invista – Best Pacific has worked with Invista since its mill’s inception in 2003 and launched one of the first lines of commercially available Lycra Sport Power-Comfort-Energy (PCE) index-certified fabrics in mid 2017.

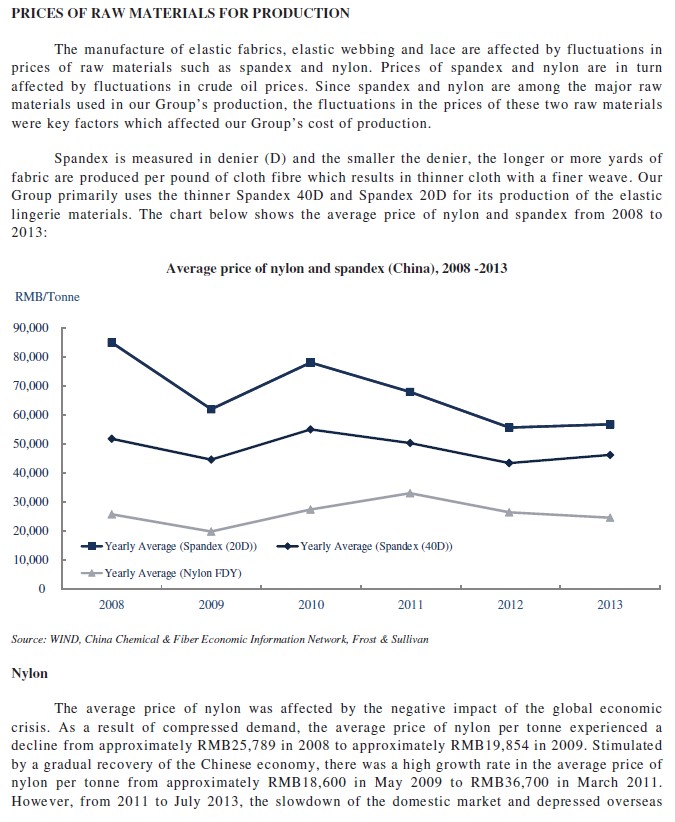

The prices of Best Pacific’s raw materials are affected by the prices of spandex and nylon, which are in turn affected by fluctuations in crude oil prices and the supply-demand economics in the market (e.g. economic crisis leading to lower demand and therefore lower prices, and oversupply in certain markets at certain times leading to lower prices). The chart below provides some idea of the prices of nylon and spandex in China, albeit for an outdated period.

Average price of nylon and spandex in China, 2008-2013

Source: IPO prospectus dated 13 May 2014.

In my view, Best Pacific is exposed to the fluctuations of raw material prices to a minimal extent only, because:

it sets its product prices on a cost-plus basis, so as long as it is value-adding (from its R&D and innovation and the quality of its products) and as long as the brands (of which most of them have quite high gross margins and branding/pricing power) or garment manufacturers are not facing tremendous headwinds, it should be able to pass on most (if not all) of the increase in raw material prices; and

according to a CICC 2016 report, “Prices of raw materials (spandex and nylon) are influenced by oil prices, while yarn providers hedge the fluctuations. The ASP has been less volatile vs. raw material prices in the past. Judging from historical financial results, the company’s sales have shown steady growth and do not fluctuate together with raw-material prices.”

This, in my view, is supported or evidenced by the company’s relatively stable and high gross margins in the past few years (2017 GPM was affected by other factors – more on the financials later), although these are historical records which do not guarantee that Best Pacific can continue to produce innovative and quality products to justify the price premium of its products.

Best Pacific’s gross profit margins

Source: Annual reports.

R&D & innovations

R&D is a big part of Best Pacific, in line with its core value of “Build on innovation and technology”. Historically, it has been spending around 2%-3% of its revenue, or HKD 38m (in 2013) to HKD 80m (2017) a year , on R&D activities.

For example, the 2017 annual report states “The Group is dedicated to catering to the changing market preferences by introducing innovative lingerie, apparel and sportswear materials. For the years ended 31 December 2016 and 2017, the Group’s research and development costs represented approximately 2.2% and 3.0% of its total revenue, respectively.”

In terms of R&D, the 2014 IPO prospectus states that “Apart from maintaining close relationships with lingerie brand owners to develop new lingerie materials, we also work closely with out major raw material suppliers, who are leading players in the nylon and spandex industries, to jointly develop new fabrics or materials in response to the evolving market demands. When a new material is jointly developed by us and the supplier, we may request the supplier to enter into exclusively arrangements with us for the supply of the jointly developed material, allowing us to capture the market demands for such new material on an exclusive basis and increase our market share in the global lingerie materials market. The costs associated with our collaborations with our suppliers on research and development are generally shared between us and the suppliers.” [emphasis mine] The company also has a design studio in Qingdao City in order to capture local talents and innovation since 2012.

As at the end of 2013, the R&D team consisted of 91 personnel who are led by Mr. Shi Jiangzhi 石蒋志, a member of the senior management team who has been an employee of the company for ~10 years then, and the company had registered for 30 patents in China which are material in relation to its business.

Three years later, as at the end of 2016, the R&D team has grown slightly to more than 100 personnel (based on a CICC December 2016 report) and the number of patents has at least doubled to more than 60, being a mix of design patents and fabric patents (as at December 2015, based on a Oriental Patron 2015 report). The R&D team is split into two teams, one working closely with the major raw material suppliers, who are leading players in the nylon and spandex (Elastane) industries to develop new fabrics and material, and another team focusing on other research and lingerie product designs. In terms of design, I have only come across data for 2013, where the company generated about a substantial 200 new designs in 2013.

Best Pacific’s R&D facilties

Source: Daiwa 2014 report.

Source: Daiwa 2014 report.

In addition, the company:

works closely with a French fashion consulting firm (since May 2012) to assist in design and advise on trends, colors, and choice of threads and materials for elastic fabrics, elastic webbing and lace products;

has also opened a School of Management and Administration in June 2016, “which aims to provide generic management training to employees of different managerial level, the first leadership and management training programme was launched during the year and external consultants have been engaged to give lectures to the relevant employees once a month since August 2016”; and

has also established a Institute of Technology and Research in June 2016, and during the year, “the Institute engaged external professionals in the textile sector to provide a series of lectures to employees of different positions. The lectures aimed to introduce updated garment design concepts, manufacturing techniques and other industry specific knowledge to the relevant employees, so as to strengthen their knowledge of textile technology and to provide them with updates on the innovation and trends of the textile and garment industry. There were a total of 60 employees from the design team, research and development team, sales team and production department attending the lectures.”

The company’s R&D activities has resulted in a few key innovations, as follows:

April 2011, Lingerie material for Victoria’s Secret: In April 2011, Best Pacific’s R&D team developed a material for bras that was granted a patent, and was ultimately selected by Victoria’s Secret for its Body by Victoria’s product line. By developing the material, Best Pacific was able to enter into an exclusivity agreement with Victoria’s Secret to supply the material to its designated OEMs from 2012 to 2014, which laid the foundation for more business.On a separate note, on Best Pacific’s relationship with Victoria’s Secret, according to a CICC December 2016 report, “Best Pacific International became a supplier of the brand [Victoria’s Secret] following a 3-year evaluation of the company’s R&D capabilities, and it now accounts for 50%, 60% and 25% of lingerie material, sportswear material and elastic webbing orders from Victoria’s Secret.” [emphasis mine] This, to some extent, shows the vigour of Victoria’s Secret’s evaluation process and the R&D capability of Best Pacific;

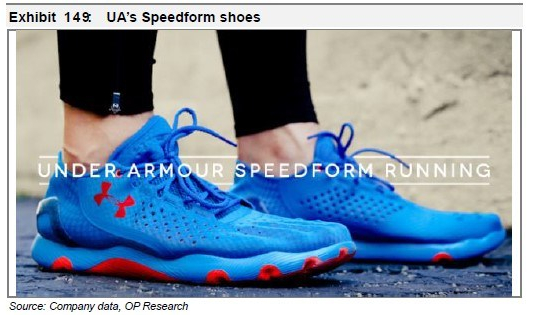

Mid 2013, Under Armour SpeedForm: In mid 2013, Under Armour launched its star SpeedForm running shoes (featuring flexibility, comfort, lightness and seamlessness) with the slogan “a bra for your feet,” signaling that core manufacturing technology could be shared between intimate wear and high- tier functional sportswear products. Best Pacific (together with Regina Miracle) was selected as the supplier of the cutting-edge materials for those shoes (the same materials that Best Pacific has developed for bras are now also being used in running shoes).A Daiwa 2014 report states that “To draw a parallel, we would compare Under Armour’s SpeedForm to Nike’s Flyknit footwear product, both of which are considered by the market as potential game changers in the footwear industry and as being highly innovative. The fact that Best Pacific beat other much larger and more experienced shoe makers like Yue Yuen to supply the SpeedForm running shoes is a testament to the company’s technological know-how, in our view. While SpeedForm was launched in mid-2013, Best Pacific was still the only supplier of SpeedForm to Under Armour at end-June 2014.” [emphasis mine]A quote from the 2015 Investor Day of Under Armour says it all: “We made shoes in a bra factory because it enabled us to do things that’s never been done before, by the level of fit and comfort that was unmatched and unobtainable in traditional footwear manufacturing facilities.” Best Pacific, joining hands with Regina Miracle, is part of this breakthrough; and

June 2017, Invista’s Lycra sport PCE (Power-Comfort-Energy) index: It was announced in June 2017 that Best Pacific, and another textile makers (Taiwan-based Eclat Textile), started integrating Lycra Sport’s Power-Comfort-Energy index criteria in their products.“In today’s global-competitive marketplace, innovation alone isn’t enough,” said Huw Williams, Invista’s global segment director, activewear and outdoor. “You also have to be able to clearly and concisely communicate to customers the advantages of fabrics employing a technology like Lycra Sport. That’s what the Power, Comfort and Energy index enables mills to do.”The new fabrics by Best Pacific leverage the recovery performance of Lycra Sport technology and Best Pacific’s high-gauge, double-knit construction to deliver a high stretch modulus that’s well suited for the high-growth active sportswear sectors. Kevin Zan, general manager of Best Pacific’s sports division, said Lycra Sport PCE, launched last year, has been a game changer when it comes to designing, producing, differentiating and selling performance fabrics.One year later, in July 2018, Best Pacific launched a new consumer-centric LYCRA® Bra Fabric Finder™ (BFF) at the Paris Mode City Show to help consumers pick the perfect casual bra. The new “BFF” consumer initiative builds on the original LYCRA® Bra Fabric Finder™ B2B program launched in 2017, which was created by INVISTA to help designers easily identify the best fabric construction and add functionality to any casual bra collection. While the list of participating mills is global, Best Pacific has built the most comprehensive collection of qualified fabrics.

Market & competitors

Lingerie (materials) market

According to a research by Frost & Sullivan, the global lingerie materials market was worth around USD 8.9 billion in 2015, and had been growing at around 5%-6% in the five years leading to that (2011-2015). Meanwhile, the output of China’s lingerie materials market was around RMB 15 billion (or ~USD 2.4b) in 2015, so around 25% of the global market.

Lingerie materials market size

Source: CICC 2016 report.

Source: CICC 2016 report.

The global lingerie materials market is highly fragmented, with a large number of Chinese and overseas players. The top five lingerie materials maker took up around 9% of the market (as at 2012). Best Pacific is the largest player overall (2.3%) and in elastic fabric (5.3%), and second largest in elastic webbing (3.9%).

Market share of lingerie materials makers, 2012

Source: Daiwa 2014 report.

The lingerie materials industry presents high barrier of entry to new entrants, mainly due to:

its capital and labour intensive nature, where large-scale investments in fixed assets, raw materials, technology, human resources and cash flow are required to achieve economies of scale. These investments include the capital investments required for setting up a factory and purchasing machineries with new technology, employing and fostering professional, technical and management personnel;

the high environmental compliance standards – with local and foreign countries attaching high importance to environmental issues, the production process involving emission of wastewater is regulated by government constraints and green barriers set by international purchasers. As a result, significant investments required for facilities to control emission of wastewater and compliance with green standards are also likely to pose difficulties for new entrants; and

the need to establish operating track record and trust with the customers, where client expansion is difficult for new entrants because it takes time to build trust with customers that demand stringent product quality and such customers have a tendency to purchase from established, qualified and authorised suppliers.

Sportswear market

Sportswear is a large and fast growing market in recent years, due to the trend to be more healthy and exercise more, and the ‘athleisure’ trend. Best Pacific’s 2016 annual report states that “global sportswear market was a supernova in 2016. According to Euromonitor International’s research report, the retail sales value is estimated to show a 7% compound annual growth rate (“CAGR”) from 2016 to 2020, as compared to about a 3.4% CAGR recorded between 2010 and 2015. “One in every six dollars we spend globally on apparel and footwear, we spend on sportswear”, quoted from a Euromonitor International’s research report, which implies the huge potential in the sportswear market and has reaffirmed Best Pacific’s intention to further expand our sportswear business.”

Overall textile market

The overall textile industry has undergone at least two major changes in the 2010s, i.e.:

manufacturers, both textile and garment, shifting their production bases out from China to other developing countries (e.g. Vietnam and Cambodia), in view of the rising and relatively higher labour costs in China – average monthly wage of USD 700-800 in China vs USD 250-300 in Vietnam (based on a Maybank 2017 report); and

industry consolidations, due to challenges in the industry, in terms of cost control and more stringent demands for shorter lead time (to cater to the fast changing trends) and better quality of production and materials (higher performance materials with various features), where the companies that are smaller or less efficient that could not adapt got squeezed out.

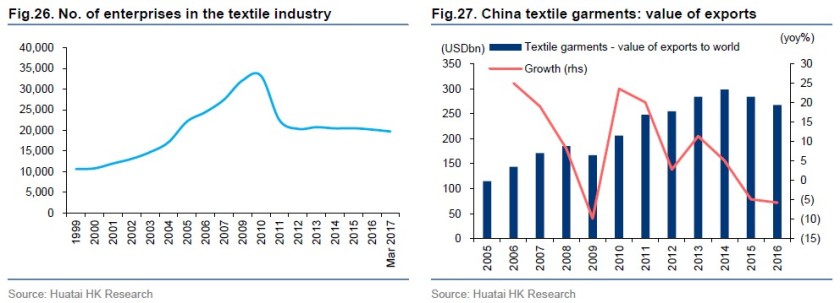

According to a Huatai June 2017 report, “Since 2010, many smaller OEMs have shut down operations due to industry consolidation, caused by the rise in labor cost and stringent requirements from brand owners in areas such as environment protection, child labor and work overtime rules. As of March, there are 19,740 enterprises in the textile industry in China, down 40% from the peak level of 33,218 in 2010. We believe the downward trend will likely persist as OEM manufacturers continue to shift to other locations with cheaper labor costs such as Vietnam and Cambodia. We understand that labor costs in some Southeast Asian countries are 50% lower than in China. Companies that can afford to relocate and those who can survive the industry consolidation are deemed survivors with strong potential to increase capacity and win orders from brand owners.”

China textile industry details

Source: Huatai 2017 report.

Competitors/market players

There are many players in the textile industry, with different characteristics, for e.g.:

upstream (yarns) vs mid-stream (fabric) vs down-stream (garment);

different focus/specialisation in terms of raw materials – natural vs synthetic fibres;

different production layout (in terms of the geographical bases); and

different business strategy, for e.g. in terms of customer concentration.

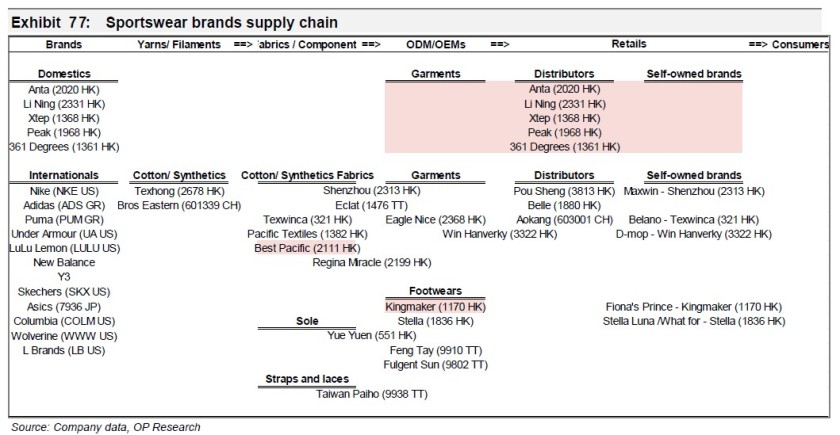

The diagram below provides a good overview of the textile value chain, and where Best Pacific sits in that chain.

Sportswear brands supply chain

Source: Oriental Patron 2015 report.

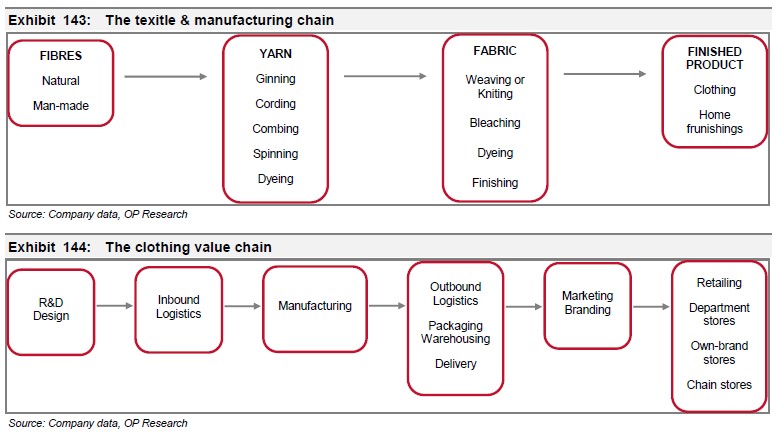

Within this textile value chain, I have a preference for the mid-stream players, as I see it as an area with potentially more companies with moats/ competitive advantages, instead of just a commodity player. Oriental Patron puts it nicely in its 2015 report, stating that “Fabric makers have the edge – We believe the fabric makers are more preferable as they are 1) less labour intensive, 2) more technological know-how is involved, especially in the dyeing process, and 3) less violable to any sudden changes in raw material prices, as they have greater bargaining power to pass on the costs. In fact, we can tell from the gross and net margins from the listed peers. The fabric makers’s average net margins outperformed at 11.8%.”

Textile and manufacturing chain

Source: Oriental Patron 2015 report.

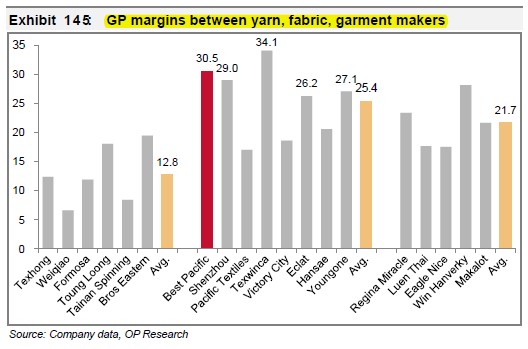

As seen in the chart below, the mid-stream players, or the vertically integrated players (from up- to down-stream) generally have higher gross margins, which are indicative of higher pricing power (and potential ability to extract economic rent).

Gross profit margins of textile makers

Source: Oriental Patron 2015 report.

In terms of Best Pacific’s competitors, each of the players (including the mid-stream ones) has different charateristics and business dynamics than Best Pacific.

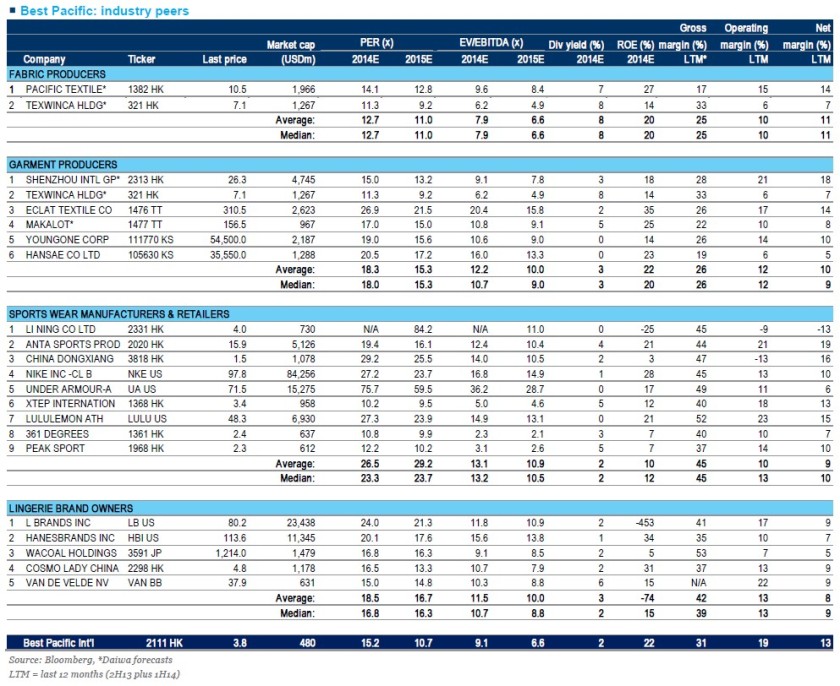

The closest competitor is probably Pacific Textiles, where they both deal with synthetic materials and have quite similar customer segments (both lingerie and sportswear) and production bases. However, Pacific Textile has lower gross margins, high customer concentration (Uniqlo and Victoria’s Secret) and low reinvestment activities (its dividend payout for past few years was 100% or more). More importantly, its annual filings have very limited information which basically make it difficult for me to understand the business and its developments, and I don’t want to own businesses that I can’t understand. However, it would be worthwhile tracking Pacific Textiles since it has some overlapping customers with Best Pacific, a different financial year end (March) and a JV with Brandix which is partnering with Best Pacific currently.

The diagrams below provide more information about the different players and their focus/ strength and customer base.

Regina Miracle is in more of the downstream side (albeit an IDM, innovative design manufacturer, which has some high value-adding activities too) and is a close customer of Best Pacific, producing the garments for Victoria’s Secret, Under Armour and other customers (Adidas, Reebok, Calvin Klein, Maniform, Champion, Bali and Warners). It has lower gross profit margins than Best Pacific, even though it is larger (should be the largest bra manufacturer with a ~1% global market share) and also spends more % (~4%)of revenue on R&D, probably due to its lower-margins downstream garment production activities. Even though this company appeals less to me, it is worth monitoring it given that it is a major customer of Best Pacific and shares similar situations with Best Pacific (similar customers and the expansion of production bases in Vietnam at an earlier time than Best Pacific).

Shenzhou International is another interesting player, where it is a very large (around 10x Best Pacific’s size) vertically integrated player with production bases in various locations (China, Vietnam and Cambodia). It has high gross and net profit margins too (comparable gross margins but higher net margins than Best Pacific due to lower operating costs due to a greater customer concentration (90% for Uniqlo, Adidas, Nike and Puma)), with high return on capital. Without having delved deep into Shenzhou International, I am sticking with Best Pacific for now (which I am satisfied with), partly due to its niche position in lingerie market which gives it a very strong hold in that market (Shenzhou does more of sportswear and general apparel, so less innovation involved, but has great advantage due to its vertically integrated model and fast lead time) and smaller size (thus benefiting from a smaller base effect). However, it’s a company worth exploring more in my opinion, as it would most likely benefit a lot from the industry consolidation.

Overall, I don’t see these big, renowned, or quality players as competing strongly with each other, as the industry is highly fragmented. The very weak or weak players would get squeezed out, which provide rooms for growth for the strong players that remain, and given that it takes time to expand and scale up production in this capital- (and for some, labour-) intensive business, there are still room for the strong players to grow in the next few years without having to compete heads-on with each other strongly. Thus, I don’t need to choose the best player, only a good enough player for my standards (this is not a winner-take-all market), that is available for purchase at a good price.

Financials

This sub-section sets out some summary financials of Best Pacific (more are covered later at the relevant places).

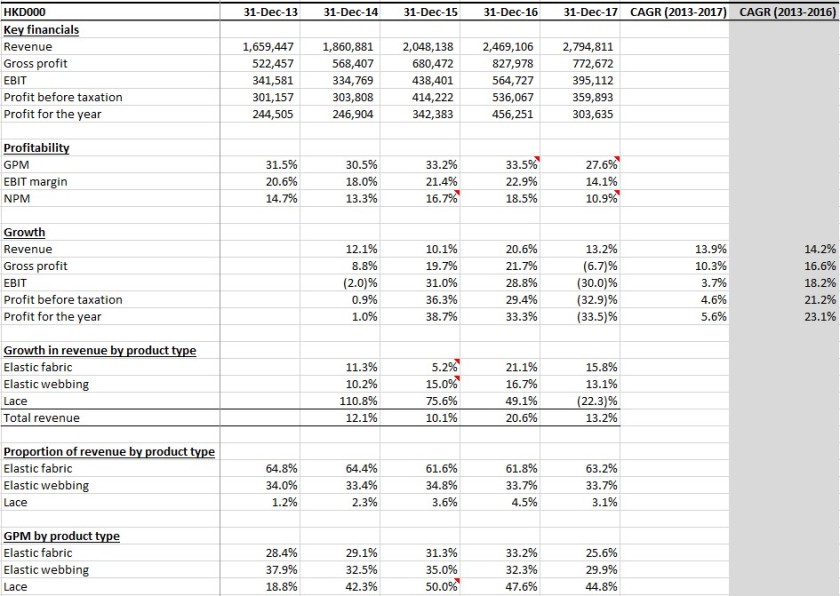

As seen in the table below, over the past four years, from 2013 to 2017:

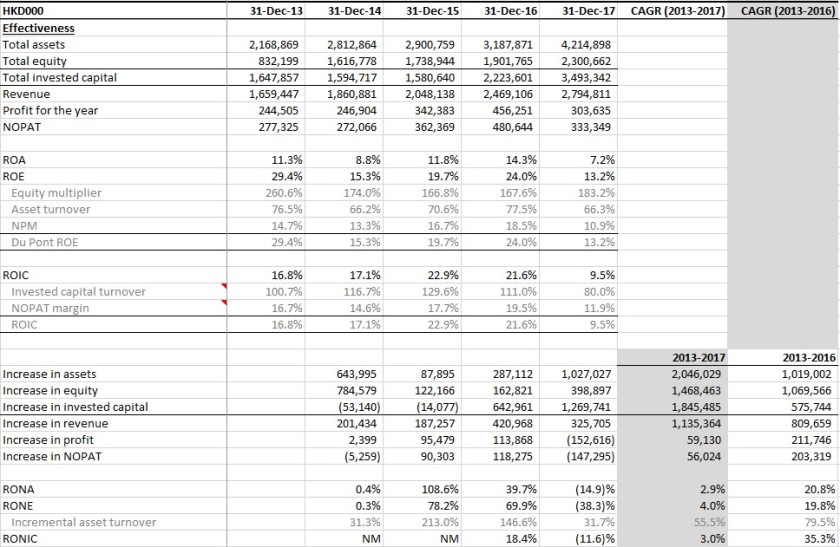

revenue has grown relatively consistently at a CAGR of 14%, from HKD 1.7b in 2013 to HKD 2.8b in 2017;

gross profit has grown at a lower CAGR of 10% and profits at a mediocre CAGR of around 5% – This is mainly due to the underperformance in 2017 in terms of profits, which I consider is an one-off depression in margins due to the start-up phase of expansion in production facilities and operations in Vietnam. The first half of the year saw assets (machineries and plants, amounting to additional ~25% production capacity) and personnel (around 500 people, or 10% increase in total workforce) being built up with no revenues at all (and additional expenses due to hiring and training of personnel and other professional expenses), until the trial production in trial production in July 2017 and official first batch production in 2017Q3;

GPM and NPM have remained relatively high at ~30% (28%-34%) and ~15% (11%-19%) or more respectively, with lace products commanding the highest GPM (45%-50%), followed by elastic webbing (30%-35%) and elastic fabric (26%-31%); and

the mix of different product categories has remained relatively stable, with elastic fabric at around two‑third, elastic fabric one-third, and lace minimally at 3%-4%.

Best Pacific’s revenue, profits, profitability and growth

Source: Annual reports.

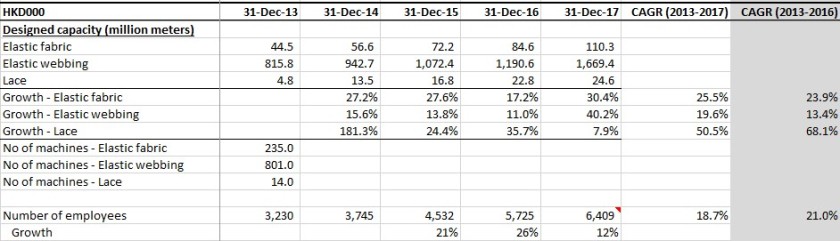

Meanwhile, production capacities have grown faster, at around 20% or more per year during the same period, while number of employees have grown by around 19%, but some of the new capacities and personnel have not been fully utilised yet.

Best Pacific’s operating data

Source: Annual reports.

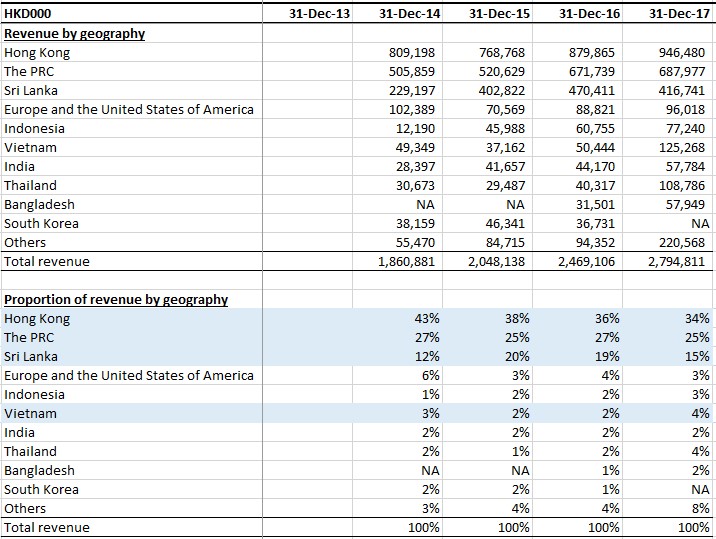

In terms of geographical location of the direct customers (not the location where the end garments are sold to), the top three based on revenues are Hong Kong (declining to 34%), China (stable at ~25%) and Sri Lanka (slight downtrend to 15%).

Best Pacific’s revenue by geography (based on direct customer)

Source: Annual reports.

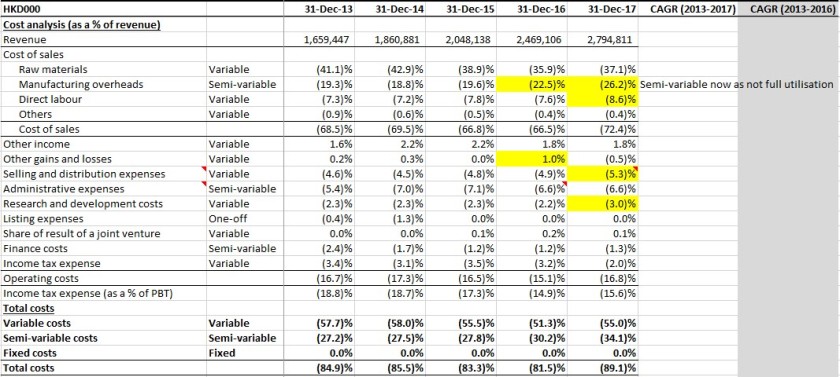

In terms of costs, total costs have been revolving around 80%-90% of revenue in 2013 to 2017, with cost of sales being 67% to 72% and operating costs being 15%-19%. There are some operating leverage for the company to tap on now at this point of time (with production capacities not being fully utilised, especially the new capacities, therefore rendering manufacturing overheads to be more of a semi-fixed nature), because as at 2017:

variable costs were around 55% of revenue; and

semi-variable costs were around 34% of revenue (with manufacturing overheads being 26%) (I have not treated any costs as fixed costs, even though they might be, to be conservative in thinking about operating leverage in a growing business context).

Best Pacific’s costs

Source: Annual reports.

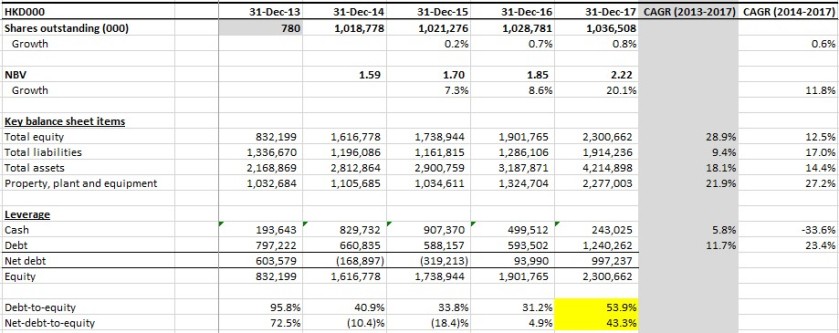

In terms of balance sheet items, from 2014 to 2017 (2013 is not that meaningful as it was before equity raising via IPO and paydown of debt in 2014):

share base has increased only slightly (due to issuance of some share options) at a CAGR of <1%;

total equity and net book value has increased at a CAGR of 12%;

total assets and PPE have increased at a CAGR of 14% and (a much higher) 27% respectively, which shows the substantial expansion in production base; and

leverage has greatly increased from net cash position in 2014 to 43% net-debt-to-equity in 2017, due to the use of cash and take-up of debt to expand production facilities.

Best Pacific’s summary balance sheet

Source: Annual reports.

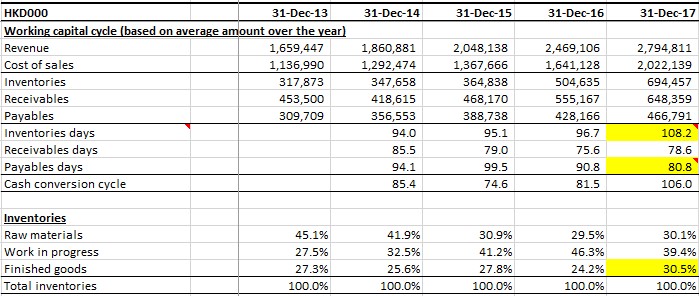

In terms of working capital, the cash conversion cycle has generally been stable, but was squeezed in 2017, due to increase in inventory days (due to brand customers demanding faster lead time, and stock up of inventory due to increased production layout in more locations) and reduction in payable days (to secure better pricing from the suppliers).

Best Pacific’s working capital cycle

Source: Annual reports.

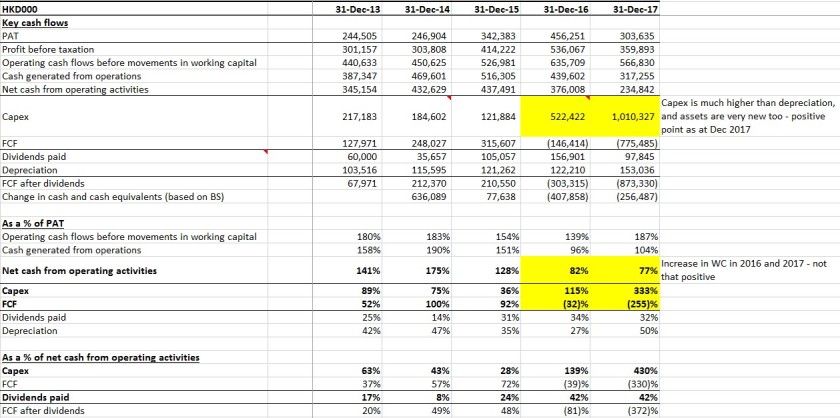

In terms of cash flows:

quality of earnings have been pretty good, with net cash from operating activities being 130% to 175% of PAT in 2013 to 2015, although this measure dropped to below 100% in 2016 and 2017 due to greater increase in working capital requirements;

the company has been reinvesting its operating cash flows a lot into capex to expand the business and production facilities, with capex exceeding depreciation by a significant margin (sowing the seeds now and reaping the rewards in a few years time, when capex slows down and goes back to a more reasonable sustainable manner, although not happening in 2018 due to the capex scheduled for Sri Lanka expansion); and

the company distributes out about half or less of the remaining free cash flows as dividends, at around 25%-35% of PAT (in line with the indicated dividend policy of at least 20% payout), and uses the remaining amounts to build up cash and pay down debt (especially in 2013 to 2015).

Best Pacific’s key cash flows

Source: Annual reports.

3. Moat

Overall

A company with high return on capital is unlikely to be able to sustain that high level of return over a long time without a strong and lasting moat, and that is not the type of company that I want to own, hence my focus on moat.

In my view, Best Pacific has two types of moat – (i) a strong moat in terms of intangibles, and (ii) a weak (or less strong) moat in terms of efficient scale.

Intangibles

Best Pacific has the following intangibles which allow it to secure existing and new customers and orders, and extract economic rent or high return on capital:

close partnership and relationship with both the customers (lingerie and sportswear brands or downstream players (e.g. Regina Miracle)) and the suppliers (synthetic fibre producers) in gathering market intelligence and developing new (innovative) products, e.g. working with:

Invista since 2003, and launching Lycra Sport PCE index-certified fabrics in mid 2017, and launching a new consumer-centric LYCRA Bra Fabric Finder (BFF) for the designers in July 2018;

Victoria’s Secret since 2007, and developing a new bra material in April 2011, of which it entered into an exclusive supply arrangement with Victoria’s Secret for three years from 2012 to 2014; and

Under Armour since 2012, and (together with Regina Miracle) developing and supplying the materials for Under Armour’s star SpeedForm running shoes;

strong production and R&D capabilities, including track record:

evidenced by Victoria’s Secret’s selection of it as one of its main supplier (in fact, the largest) after a 3-year evaluation of its R&D capabilities and presumably its quality products, becoming the largest global lingerie materials maker in a short period of 10 years (it was already the largest when it IPO‑ed in 2014), and securing of major global brands including in sportswear despite its new entry; and

supported by its continuous large spending on modern machineries from European companies (of approximately HKD 0.2m-5.3m per machine, from Karl Mayer and Miller) (with the total PPE now worth HKD 2.3b at end 2017), and substantial spending on R&D (HKD 84m in 2017, or 2%-3% of revenue in the past few years, among the highest in the industry compared with other leading players) with a substantial team (>100 employees, or around 2% of total workforce);

a pool of innovation and design inventions and patents developed over the years – more than 60, in terms of both design and fabric patents, as at end 2016 (which doubled from the 30 three years ago in end 2013), and substantial amount of new designs every year (200 new designs in 2013); and

a certain level of branding within the industry, for its quality (and pricier) products – according a Daiwa 2015 report, its “market research with multiple players along the lingerie value chain shows that Best Pacific is known among its peers, suppliers and customers for its high-quality but often pricier fabrics” [emphasis mine].

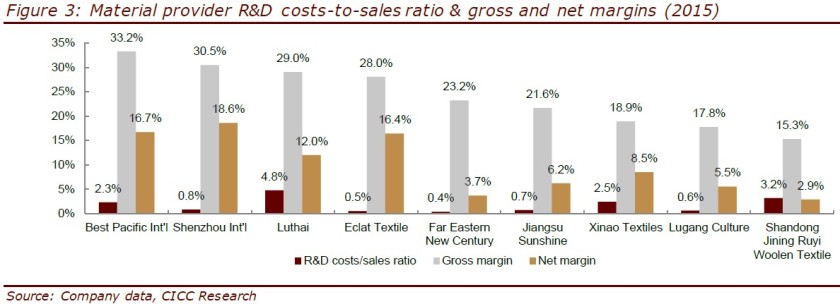

These intangibles (relationship, R&D, product quality, innovations and branding) have allowed Best Pacific to secure existing/new customers and orders, and charged a premium on its products, evidenced by its high gross margin (the highest in 2015 compared to some leading peers), as shown in the figure below.

Leading textile players’ R&D expenses and profit margins

Source: CICC 2016 report.

Although Best Pacific has a strong moat in terms of intangibles currently, which is good, it is also important to figure out the moat trend for this moat, i.e. whether it would become stronger, remain the same, or become weaker in the future, say in the next 5 to 10 years.

In my opinion, Best Pacific is still up-ing its game in R&D and innovations, given:

its active decision to increase R&D spending (a higher 3.0% of a higher revenue in 2017, vs. the previous low 2.2%-2.3%, although this increase was partly driven by demands from the brands side);

its recent launch of Invista Lycra Sport PCE index-certified fabrics last year (mid 2017) and LYCRA Bra Fabric Finder (BFF) for the designers recently (July 2018) of which it has the most comprehensive collection of qualified fabrics among the participating mills; and

its recent strategic collaborations with leading downstream players in Sri Lanka (Brandix and MAS) to produce synthetic fabrics;

and therefore I think that this strong intangibles moat of Best Pacific should remain at least as strong, with optionality for an upward improvement.

Efficient scale

Best Pacific has a weak (or less strong) moat in terms of efficient scale in the lingerie segment, where the niche lingerie segment (with a much smaller total addressable market) has not been a focus of the larger textile players which focus more on the general apparel and/ or sportswear segment (with higher growth).

Best Pacific’s focus on this niche lingerie segment in the first decade of its founding has allowed it to become the leading players in the lingerie field, being the world largest lingerie materials maker (albeit still a small 2% to 3% overall market share).

As a result, as of now, Best Pacific is more established than the other players, both in terms of breadth (where it deals with all three major components of a lingerie – elastic fabric, elastic webbings and lace) and depth (know‑how, R&D, capital and PPE investments, and human capital required to run this business well). This presents a strong edge (and opportunities) for Best Pacific, because: